In what follows, all money amounts are expressed in billions of dollars

In recent articles we have covered Apple, Amazon, Tesla and Zoom. We have seen that we need to be ready to accept a low rate of return, and to wait a long time before receiving it, before investment in any of these companies make sense. Sense, that is, in terms of how the cash flows they have generated in the recent past need to grow to justify the current valuations. For most investors in these fashion stocks, the underlying cash flows are of much less concern than the ebbs and flows of market sentiment.

Today, we are going to look at a company whose share price is much more closely connected to its underlying performance. Rio Tinto is one of the UK's best known mining companies, with interests ranging from Latin America to Mongolia.

Enterprise value

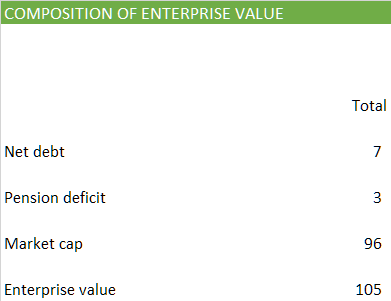

Our first step is to work out Rio Tinto's enterprise value. Normally, we do that by combining

how much the company's lenders are owed by the business, which we determine by studying the balance sheet

how much the company's investors have at stake in the business: many online data sources report this market capitalisation, along with the share price

In this case, there are two wrinkles.

Like many firms that have been in business for a long time, Rio Tinto has accumulated a pension deficit. It owes 3.1 to former employees who have now retired. Pier Analysis considers that to be just as much a debt as anything owed to a bank. We therefore include this quantity in the enterprise value. Not all analysts choose to do this.

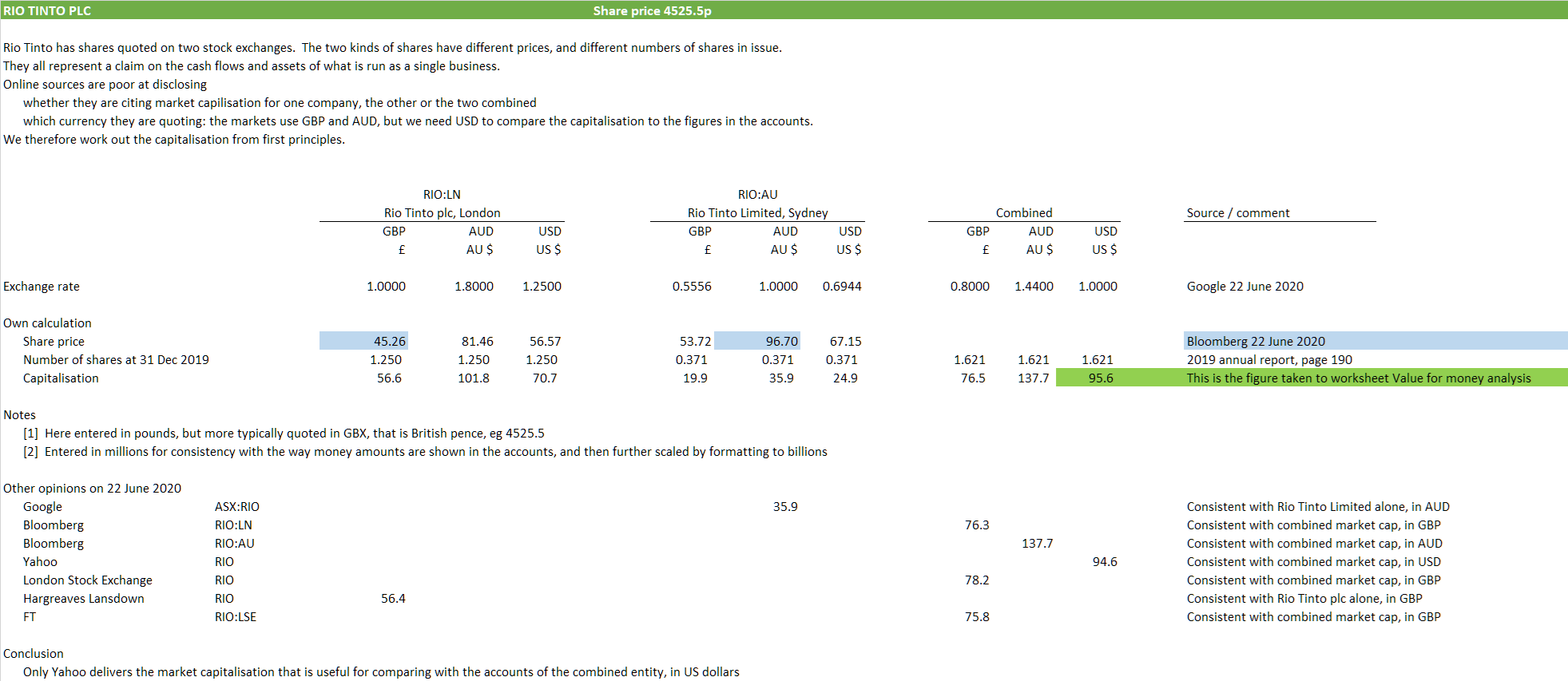

The market capitalisation is a bit harder than it looks in Rio Tinto's case, to the extent that many sources make a mess of it.

Google thinks it's 36.4.

Bloomberg reports it as 77.5.

Yahoo finance says 94.6.

The reason is that Rio Tinto has two kinds of shares, one traded on the Stock Exchange in London, called Rio Tinto plc, the other listed in Sydney, and called Rio Tinto Limited. The first is quoted in pounds; the second in Australian dollars. What we need is the two capitalisations combined, since both sets of shareholders have a claim on the cash flows of the company. And they need to be converted into US dollars, since that is the currency in which the accounts are presented.

The different sources give wildly different answers, because they treat this topic inconsistently. Some of them present the capitalisation of just one of the two classes of share rather than both. A number of them express the values in currencies other than the desired US dollars. Rather than trust any of them with this calculation, we have done it ourselves from first principles on the worksheet called Market capitalisation.

Click to enlarge

By this means, we are able to rationalise the different figures that the various electronic feeds deliver, and we arrive at an enterprise value for Rio Tinto of 105.

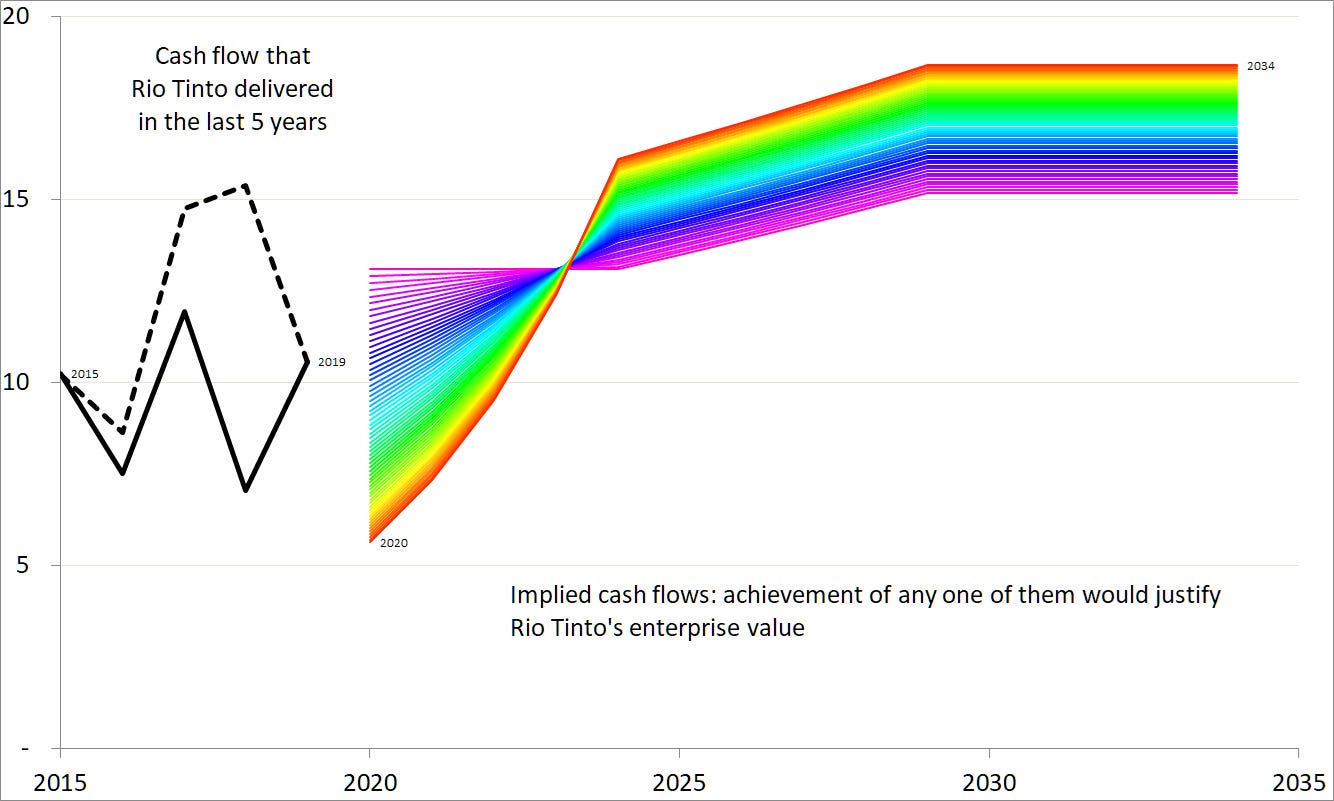

Implied cash flow

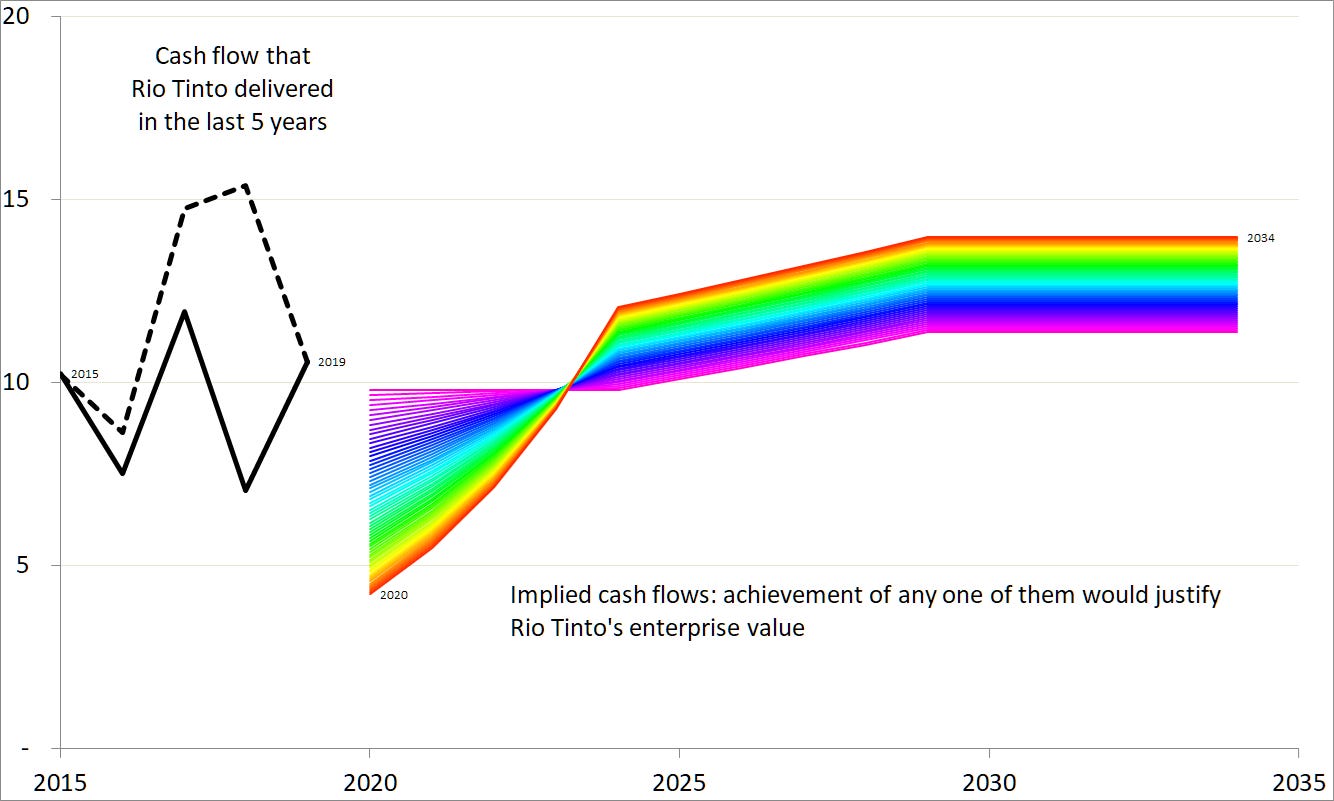

When Pier Analysis hears that a company has an enterprise value of 105, it hopes to find that it is generating cash flow of around 10, because that's what you get when you apply to the 105 the 10% rate of return that Pier Analysis favours. Actually, we would like it to deliver rather more than that, because we desire not only a return on any capital that we invest, but a return of that capital too, and we look to receive it within just 15 years.

Something in the neighbourhood of 13 to 15 would do nicely. That's the violet line on the graph. Or, if that's too much to ask, we could start lower, as long as we compensated by finishing higher. That possibility is represented by the red line, which grows from 6 to 19.

Either of these cash flows would justify the 105 enterprise value of Rio Tinto, and so would any of the ones in between, because every one of them delivers that sum in NPV terms when discounted at 10% over 15 years.

Actual cash flow

Now that we have some idea of what we are hoping for, we can see what Rio Tinto has actually produced. As the black line in the graph shows, its cash flow has hovered between 8 and 12, which is not far off what we are hoping to see.

The enterprise cash flow that Rio Tinto actually delivered is shown in the dotted line, and the black line shows what it looks like after it has been subject to various adjustments to remove items that cannot be depended on to recur.

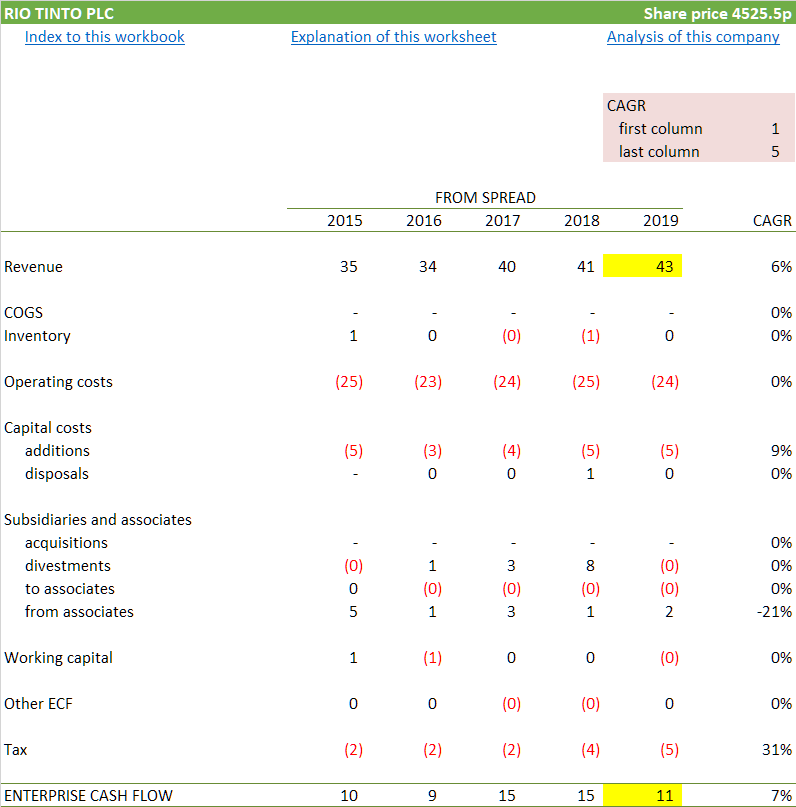

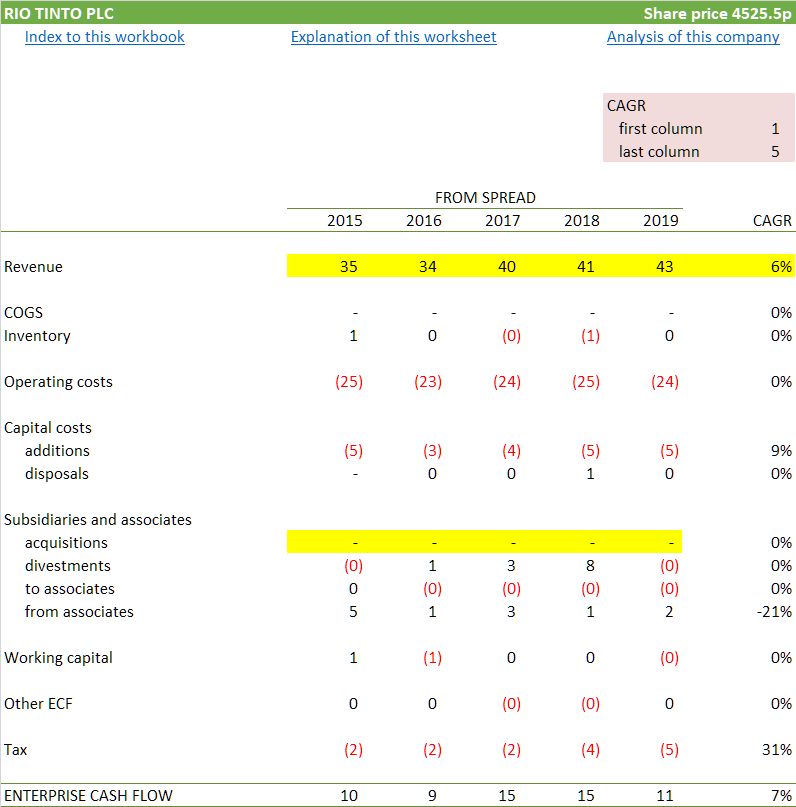

These black lines are derived on the worksheet Direct cash flow. And what a remarkable cash flow it is. Even after meeting all of its capital costs and taxes, Rio Tinto manages to keep as enterprise cash flow 11 out of the 43 that it records as revenue. That is 24%. In past years, it was even higher, above 30%. For Apple the equivalent number is under 20%, and yet Rio Tinto has none of Apple's advantage in shipping any of its product in digital form at near-zero marginal cost. Every ton of the ore it produces is trucked and crushed and piped and shipped physically to its market.

Those revenues of Rio Tinto grow at a steady 6%, and are organic; it has achieved none of it by spending the shareholders' money on acquiring other businesses

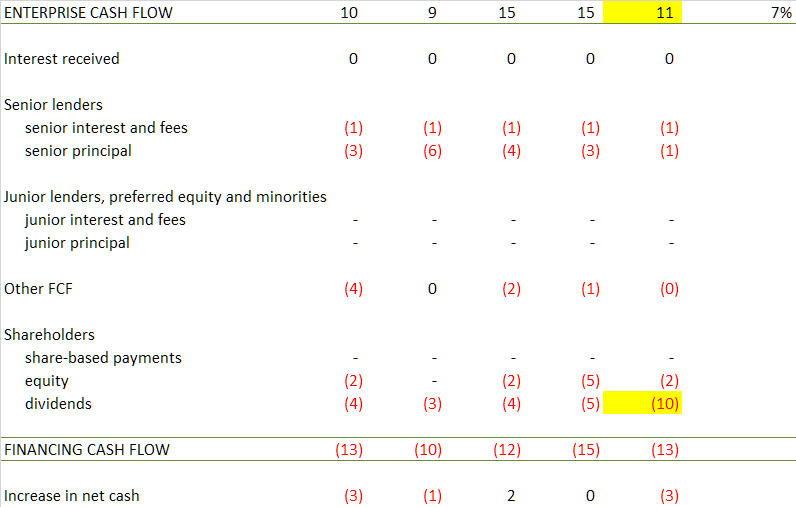

The financing cash flow is as remarkable as the enterprise cash flow. Because Rio Tinto's debt is modest and costs little to service, nearly all of the enterprise cash flow reached the shareholders in the form of dividends. Contrast that with the tech giants who have amassed cash piles of hundreds of billions of dollars and have yet to distribute a cent in dividends to their owners.

It has to be admitted that the dividend payment was not normal; Rio Tinto paid a special dividend in 2019. It is not planning to repeat that feat in 2020, so dividends will fall back to the 5 or so that they ran at in previous years. Even at that lower level, the dividend yield is around 6%.

Dependable?

These numbers give every impression that Rio Tinto doesn't have to lift its cash flow far from recent levels for its valuation to be justified. But is that impression reliable? Can Rio Tinto be depended on to repeat the performance of recent years, still less to improve on them? Attractive dividend yields are often an indication that investors expect that the dividend can't be sustained and will have to be cut or eliminated.

Nothing in this analysis reflects the effect of the Covid panic, which may have reduced both demand for Rio Tinto's products and the firm's ability to supply them. Will that effect be large? Will it last long? Such coverage as there is of this subject suggests that Rio Tinto may be finding the pandemic a benefit. The net effect is for you to judge, but it's a topic that was not worth devoting any time to considering before you gained this understanding of how Rio Tinto's performance and valuation are connected.

In March this year Rio Tinto's market capitalisation was not 96, as now, but just 69. At that price, the cash flows needed to justify the valuation are quite a bit lower, and were very plausible extrapolations of the historic cash flows.

That was at least partly the result of the Covid sell-off, which made many stocks appear cheap so long as you ignored the effects of the confinement. Those brave enough to discount the moment's news and look at the maths will have been rewarded by a 40% rise in Rio Tinto’s share price since that time.

They do exist

Holding out for a higher return on investment than is usual, and being willing to wait for only a limited period to get it, are characteristics of Pier Analysis's approach that differ from most research. Some will say that these criteria are so demanding that nothing will satisfy them. To those people we offer this note as a counterargument. It is possible to find businesses with valuations that are relatable to the underlying economics.

What next?

A distinctive feature of Pier Review is that it provides the financial model that underpins each analysis. To receive the spreadsheet

if you have not done so already, subscribe to Pier Review by using the box below

click here to pre-populate a message in your usual email program requesting that the spreadsheet be sent to you

switch to your email program and click Send to despatch the request.

If you find this analysis interesting, you can sign up to have others like it delivered to your inbox several times a week.

Share Peer Review with interested friends.