DX (Group) plc

Our second delivery turnaround, this time led by a team that's done it before.

Would you trust a lawyer to post a letter?

Our last newsletter began an investigation of the possibility that businesses delivering parcels will benefit from higher volumes as individuals confined to working from home order more items online. It looked at Royal Mail, and saw that it is at risk of strikes threatened by its unionised workforce.

It was during such strikes in the 1970s that what is now DX (Group) plc was formed. It was privately owned by legal firms wanting to be able to continue to exchange drafts of agreements and court documents while the regular mail was not operating. For some time nearly every law firm in the UK had a DX account code, and printed it on its stationery. If you haven't heard of DX codes before, you will likely notice them now when you next receive a letter from a lawyer. Since formation the company has changed hands at least once and is now a separate business.

DX makes an interesting comparison with Royal Mail. In both businesses, a portion of the income comes from the delivery of letters, and those are being displaced by email. Both have managements who talk about improving their results by shifting away from letter deliveries. In Royal Mail's case the word is transformation, which appears 84 times in its annual report. DX prefers turnaround, which appears 47 times.

DX differs from Royal Mail in that it

is much younger, being established in 1970 rather than 1516, and so being less encumbered by a venerable history

is much smaller, about 30 times by revenue and about 18 times by value

has its shares listed on AIM, the Alternative Investment Market, rather than the main London exchange.

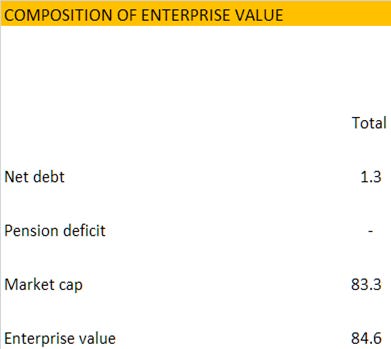

Enterprise value

Examination of DX's balance sheet shows that it has

(£3.1m) of debt, offset by

£1.8m of cash

If we combine …

this £1.3m of net debt

the value of DX's equity, being the £90.4m market capitalisation implied by the 14.52p on 3 August 2020.

… then we find that DX's enterprise value amounts to £84.6m.

Necessary cash flow

Once we know its enterprise value, we can work out how large are the cash flows DX needs to generate to justify that value [1].

One way is to deliver cash flows around £10.5m to £12.2m: this is the violet line on the graph below. Another way is to accept a cash flow that is lower than this range in the early years, say £4.5m, but makes up for that by growing rapidly so that it is significantly higher in the later years, reaching £15m. This is the red line on the graph.

And there are infinitely many contours between these two examples, and beyond them.

If the cash flows that DX generates in the future follow any of these lines, the benefits of holding a stake in the company (our entitlement to our share of these cash flows, discounted back to today) match the cost of buying that stake.

Actual cash flow

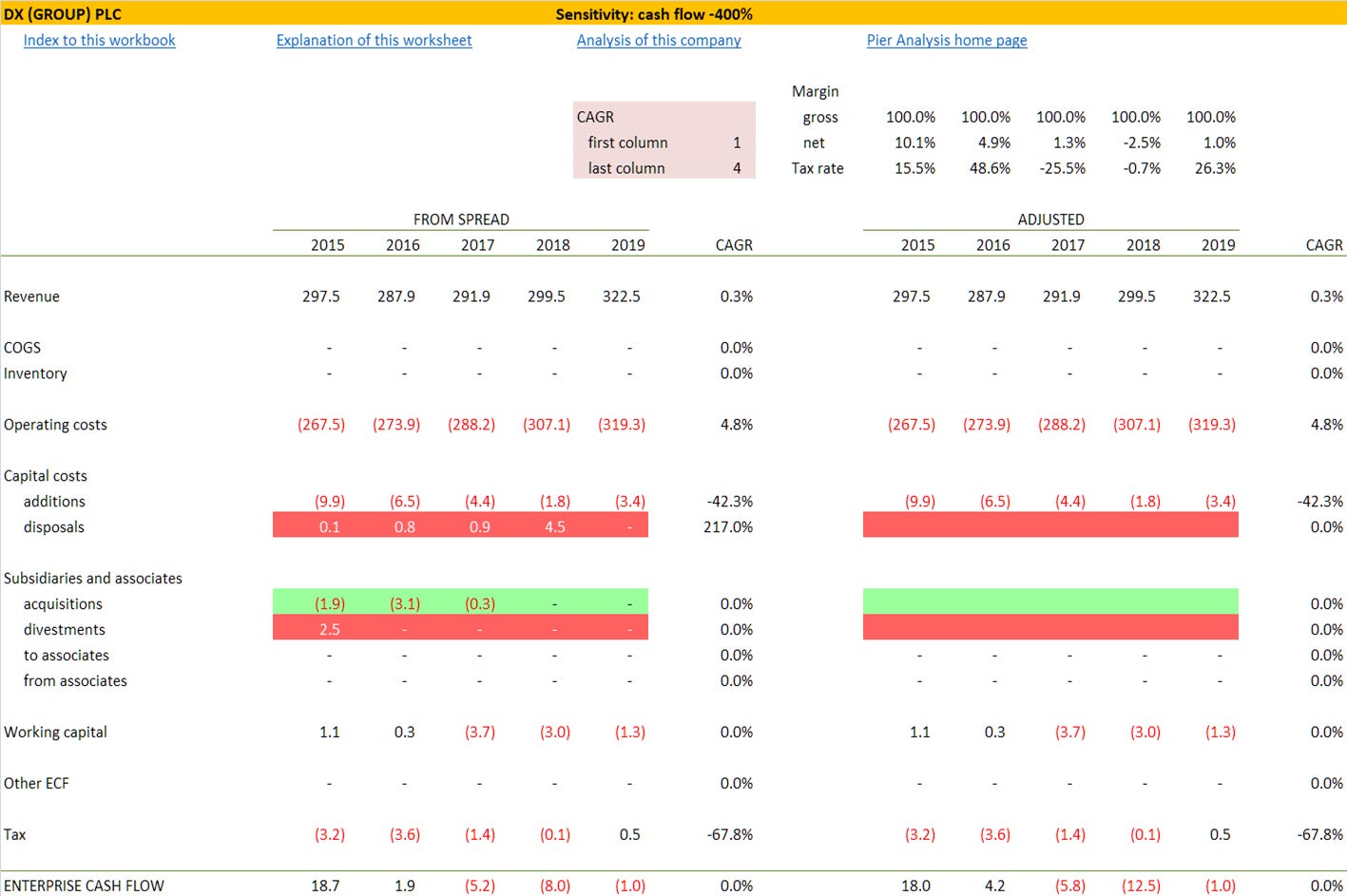

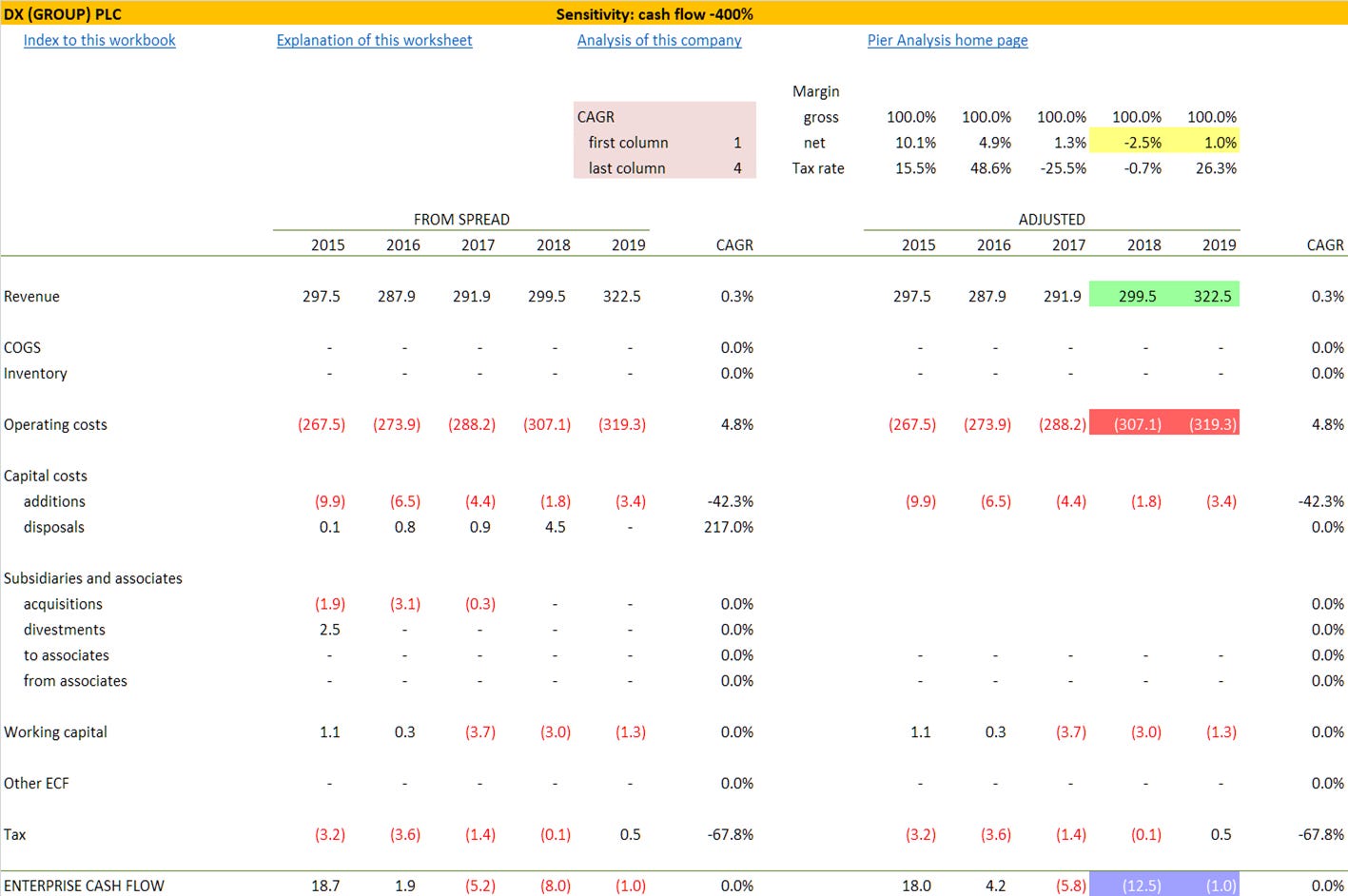

Now that we know what DX needs to achieve to reward us appropriately and return our capital to us, we can look to see what the company has actually managed. The lines at the left in the graph above show what DX’s enterprise cash flow looked like in the last five years. There is

a grey line, which is what the accounts show

a black line, which reflects what the cash flows would be after some necessarily subjective adjustments aimed at stripping out items that are unlikely to recur in the future.

The main such adjustment is the removal of the costs of acquiring subsidiaries; they have been acquired now, and will contribute to future cash flow without the cost of doing so needing to be repeated. These are the items shaded green in the cash flow extract below.

In the opposite direction, we have eliminated the proceeds that DX gained from divesting unwanted subsidiaries and disposing of surplus fixed assets: these are the items shaded red.

What we find is that

DX generated respectable cash flow approaching £20m five years ago, but it has collapsed, turning sharply negative [highlighted blue in the cash flow extract below]

The reason for that is that, between 2015 and 2018, the firm's revenue went up by less than 1% [highlighted green] but its cash costs rose by 15% [highlighted red].

the inevitable result is the eradication of the firm's margins [highlighted yellow]

During 2019, the firm clawed back 3.5 points of margin [highlighted yellow in the next cash flow extract], as its revenue rose by 7.7% [highlighted green ] but its costs only 4.0% [highlighted red]. The payoff was a sharp reduction in the cash outflow [the blue figures].

New dawn?

Is this the start of a recovery? The management would like to think so. DX's financial year ended at end of June. The annual report has not yet appeared. The most recent report was the interim, to December, which said that the "benefits of the turnaround strategy are continuing to come through "

What exactly is this turnaround strategy? It is to deemphasise the delivery of letters and small packages, and to specialise instead in delivering heavy, awkward loads for businesses. Its fastest growing segment is relieving corporate customers of their delivery burdens altogether, running their logistics for them. The legal documents delivery which was the firm's origin is only 1% of revenue nowadays.

This of course was before the Covid outbreak. Even in December, well before most firms, the DX Board was "monitoring the situation regarding the "coronavirus and its potential effects on the UK economy and the supply chain of" customers, and consequently on DX volumes." It believed it "prudent to expect a slight softening in volumes in the remainder of this financial year. DX is nonetheless expected to make further significant operational progress in H2 and to return to pre-tax profit"

This sounds optimistic. Even if volumes have held up, Royal Mail reported that it suffered noticeably increased costs to conform with social distancing and equip its workforce with protective equipment, and the same is likely true of DX.

And DX isn't particularly aiming for the kind of box shifting involved in fulfilling Amazon orders, so the premise that we started this article with, that delivery services will benefit from the Covid confinement, likely does not apply here.[3]

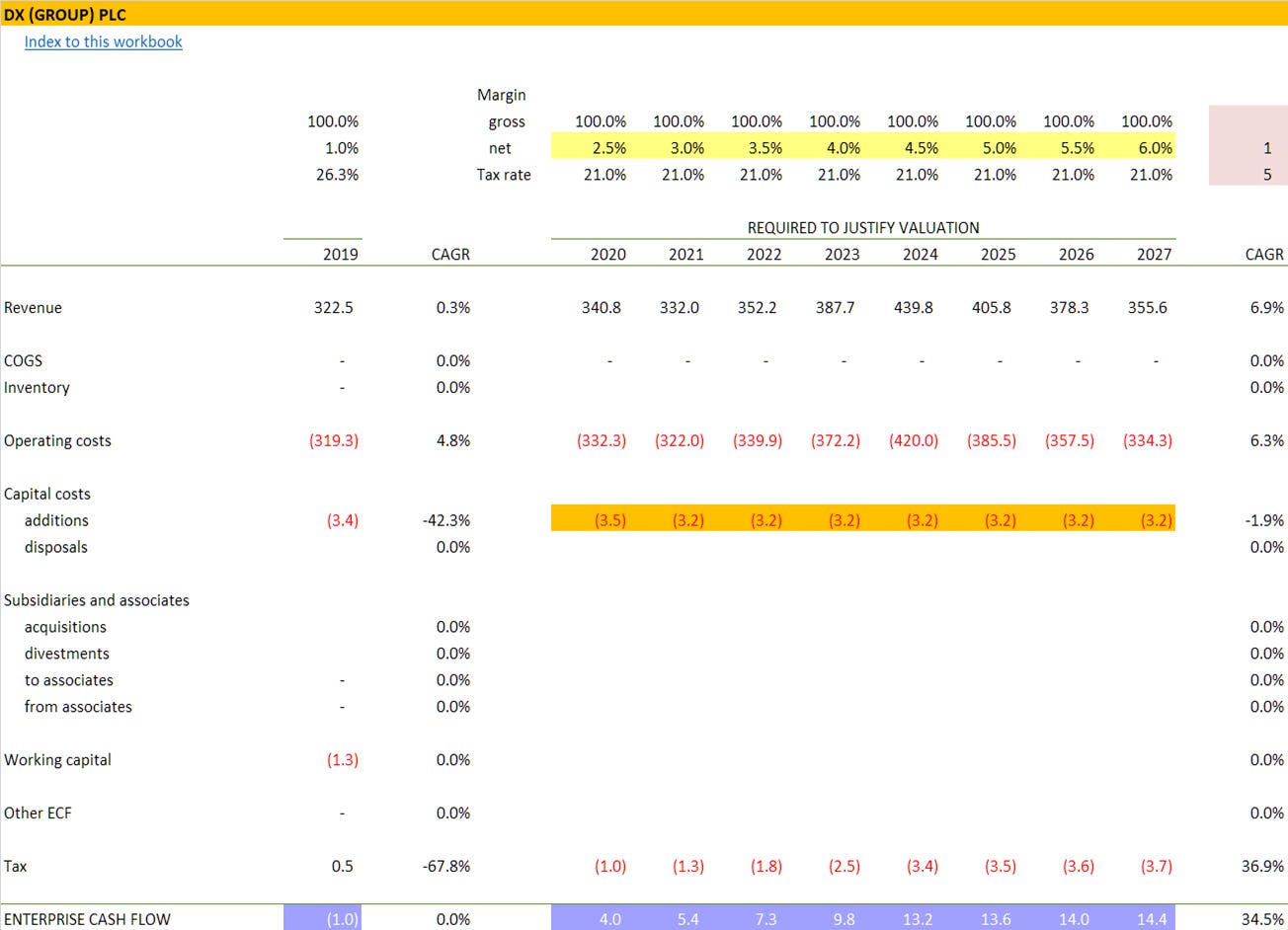

But let's give it the benefit of the doubt. If DX's recovery is on track in spite of Covid, what might it look like? On the right side of the direct cash flow in our financial model, we extrapolate the key components into the future.

Unlike most analysts, we don't attempt to estimate what the company will achieve in the coming years. Instead, we work out what the company needs to accomplish if its current valuation is to make sense.

We find we can produce a cash flow that justifies the valuation [1] if we assume that

DX can transform the negative cash flow it experienced in 2019 into a positive one of £4m in 2020; from this starting point in 2020 it then grows at 34.5% pa for five years, before levelling off [highlighted blue in the cash flow extract that follows]

margins [2] improve from 1% in 2019 to 2.5% in 2020, and on to 6% by 2027, which is still not much more than half what they were in 2015 [highlighted yellow]

capital expenditure runs at £3.2m pa, the average of the last three years [highlighted orange]

With the margins improving, cash generation growing at 34% pa demands revenue growth of only around 6.9%, which is well within the 7.7% revenue growth achieved last year.

Trading update

Though the 2020 results aren't out yet, management gave an indication of what they are like in a trading update on 14 July. The firm's cash position has moved from net debt of £1.3m a year ago to net cash of £12.3m now, but that is flattered by "payment deferrals of £11.9m in total, including VAT and other agreed payment holidays."

The net of these items is £0.4m of cash, which means that it has generated £1.7m of cash during 2020. That will be after paying interest. The measure of cash flow that we focus on, the enterprise cash flow, is measured before subtracting interest, since it is out of the enterprise cash flow that interest is paid. Assuming DX's interest in 2020 was much as it was the year before, £0.4m, we can see it generated a little over £2m of enterprise cash flow.

Sadly, that's not quite as much as the £4.0m that we conjectured as part of our valuation-justifying scenario, suggesting that the opportunities available to DX are fully reflected in the price already for anyone who shares our required rate of return and time horizon. If the share price fell, we might well have a different opinion.

DX or Royal Mail?

Comparing DX with Royal Mail, the subject of our last newsletter, we conclude that the performance demanded of the two by their current valuation is a little more plausible for Royal Mail than for DX.

But DX does have a team in place, with a chief executive who has managed a comparable turnaround before and seems to be broadly on track with this one. Royal Mail, by contrast, has lost its Chief Executive and there is no news yet about if finding a new one.

Against this has to be set the size of DX. A graph of its share price is not random and wiggly, but marked by distinct horizontal and vertical or diagonal lines.

Those straight edges are a sure sign that trading in the share is thin enough for the effects of individual transactions to be visible. That in turn will widen the bid-offer spread, the gap between the prices at which brokers sell and buy the shares to make their margin, which increases the amount by which the shares need to rise before one has covered the cost of buying them. As a rough rule of thumb, a company needs a market capitalisation of at least £250m to be free of this effect, and DX has a third of that.

What’s next

A distinctive feature of Pier Review is that it provides the financial model that underpins each analysis. To receive the spreadsheet

if you have not done so already, subscribe to Pier Review by using the box below

click here to pre-populate a message in your usual email program requesting that the spreadsheet be sent to you

switch to your email program and click Send to despatch the request

If you find this analysis interesting, you can sign up to have others like it delivered to your inbox several times a month.

Share Pier Review with interested friends.

Notes

[1] By justifying the valuation, we mean we require DX to be able to generate future cash flows that have a present value equal to £84.6m, DX's enterprise value, when discounted at 10% pa over 15 years. Any one of the cash flow profiles discussed would put DX in the position to return our investment within 15 years and give us a 10% return while we wait for it.

[2] The margins shown differ from the ones that would be typically shown as they are based on the cash costs, consistent with Pier Analysis's attachment to cash flows and disinterest in profit-based measures of cost.

[3] Counterargument: The 14 July trading update suggests that the company's volumes "are experiencing a business mix slightly more weighted to B2C than previously anticipated", so perhaps Covid has slightly perturbed this strategy.

[4] The exhibits in this article are yellow. In most of our newsletters, they are green. What this colour change is signifying is explained here.