Tracking parcels

Covid-19 has placed the world under house arrest, to the benefit of online retailers such as Amazon. One might wonder whether the increase in deliveries to households has boosted activity in firms such as Royal Mail which do the physical shifting of these boxes to the home. In this article and the next one, we will look at companies in this line of work, and see what their current valuations imply by way of expectations of the future.

Even if delivery businesses are now seeing good times, it does not follow that they make attractive investments. Any benefit, if there is one, may already be reflected amply in the company's share price. Only if we do some basic maths can we form a view one way or the other. An opinion without that analysis behind it is not worth anything.

From public to private

A letter in the United Kingdom carries a stamp bearing a picture of the Queen's head [1].

It is typically placed in a letter box which carries her insignia, or that of one of her ancestors.

None of that stopped the government from privatising the post office in October 2013, such that it moved from a department of government to a private business with shares traded on the stock market under the name Royal Mail plc.

The shares were offered at £3.30 a share, and rose almost immediately to £4.55. Forests were felled to print the newspapers which cried out that what had been taxpayers' property had been sold off too quickly. It cannot have been a comfortable time for Vince Cable, the minister in charge at the time of business, and therefore of this flotation. Disobligingly for Vince, the price touched over £6 at its peak.

Partial transformation

Using exactly the techniques described in this newsletter, the Pier Analysis team looked at the figures for Royal Mail at the time and formed the view that the newspapers were wrong. The offer price made sense so long as Royal Mail could be expected to generate cash flows of a certain size. Royal Mail was already generating cash flows on that scale, but it was spending them on what it euphemistically called transformation costs, as it moved from a state-run department, full of history and traditional working practices, to face the modern world.

The prospectus contained the sentence that

The key elements of Royal Mail’s Transformation Programme are expected to have been substantially completed by the end of FYE 2014. [2]

If this was so, the transformation costs would come quickly to an end, and Royal Mail would be worth the IPO price. If the costs continued, it would not be. The prospectus held out the first possibility. The Pier Analysis intuition was that the second one was more realistic.

So it has proved. Six years on from the share issue

the transformation costs continue, to the point that management has at last recognised that they are such a fixture that there is no longer anything to gain from disclosing them separately

the word “transformation” appears 84 times in the 2020 report and accounts

far from any end being in sight, “We remain committed to our UK transformation programme and a substantial level of capital expenditure required to achieve it.”

the share price is less than half the issue price, and less than a third of the peak.

Enterprise value

Let's have a look and see what the numbers tell us now.

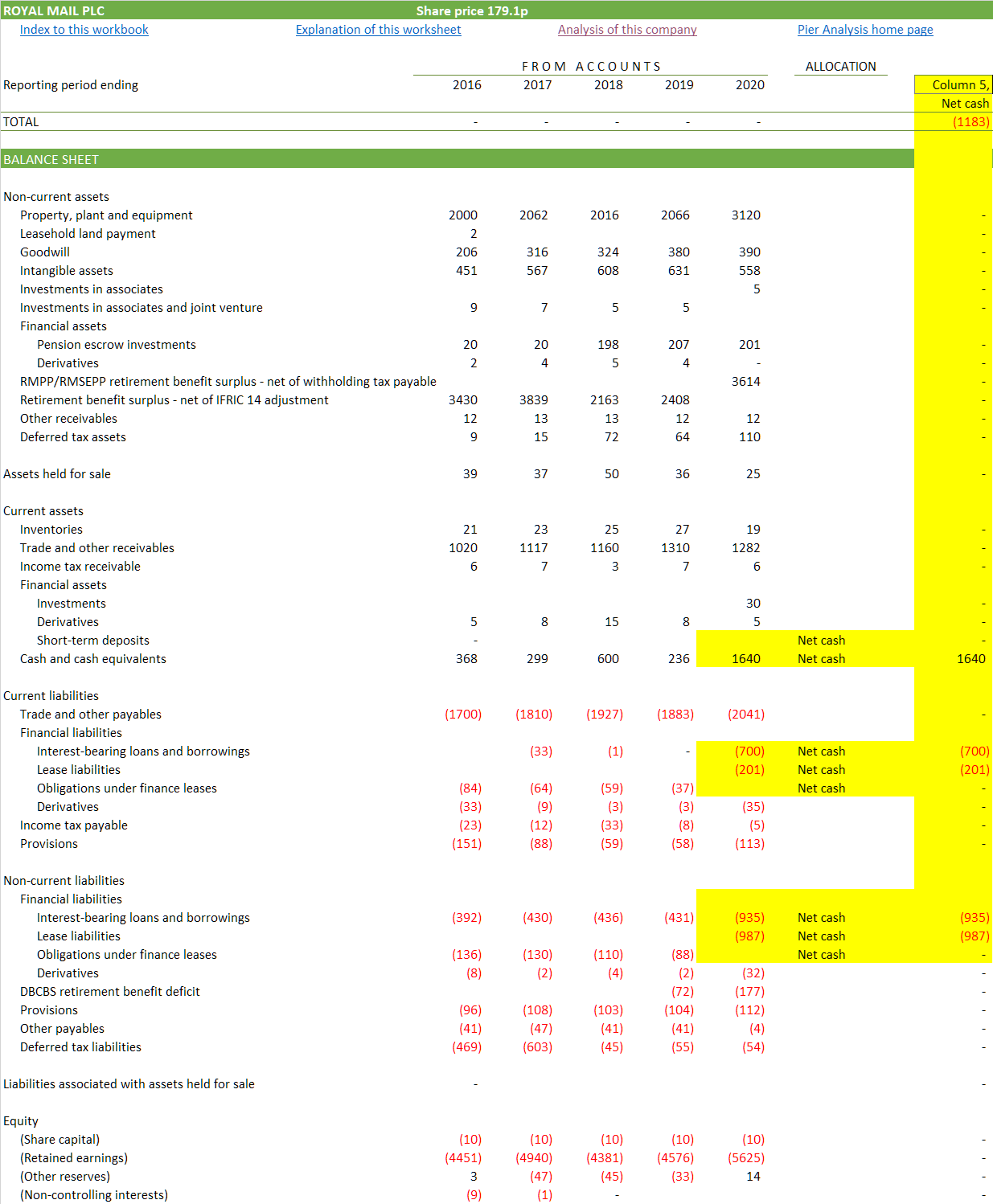

First, we go through the entries in Royal Mail's balance sheet line by line, to work out its net debt. We find it amounts to £1,183m. [3]

In past years we would have include in this total the company's pension deficit, because a liability to former employees is as much of an obligation as any other kind. Recently, the company has restructured its pension arrangements, and appears to be running a surplus. Such things can disappear as fast as they appeared, so we have chosen not give the firm credit for it. We recognise that penalising firms that have pension deficits while not rewarding ones that have surpluses is inconsistent, but we are here to make pick out companies that are priced with high margins of safety, not to treat everyone with academic fairness.

To the amount the firm's lenders have at stake in the firm, we add what the firm's shareholders have at stake, that is, its market capitalisation. Today, that is £1,790m.

Take these things together, and we find an enterprise value of £2,973m.

Implied and actual cash flow

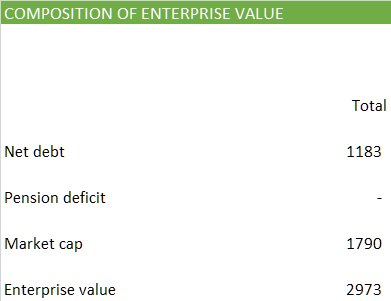

Holding a stake in Royal Mail makes sense as long as we believe it can generate at least this much cash in the coming years. As well as generating the means for the gradual return of our capital, we want a return on it while we wait. Any of the coloured lines in the graph accomplish this feat. We get our money back over 15 years, and earn a return on top of that of 10% pa. [4]

The lines at the left show what Royal Mail has achieved in recent years. The grey one is what the accounts show, and the black one is the result of adjusting the figures to remove items which are not expected to recur.

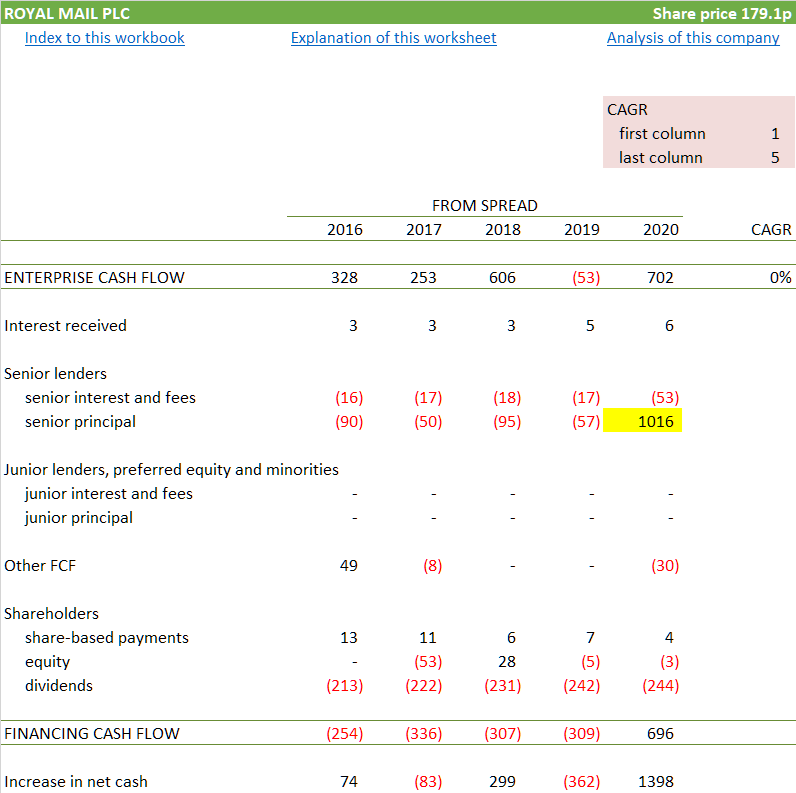

These adjustments shown in yellow in the cash flow below, are

the exclusion of acquisitions: the businesses concerned have been incorporated into Royal Mail, and Royal Mail does not need to spend the same money again to gain the benefit of them

divestments: the business units concerned have been sold off, and Royal Mail can’t get the benefit of selling them a second time

working capital, which ebbs and flows from year to year, but is broadly neutral over time

We can see in the bottom right of the table that Royal Mail has been generating cash flow that has a very decent rising trend over the last five years.

Interpretation

Unlike the technology firms which have delivered tiny cash flows in the past, but need to generate large ones in the future to justify their valuation, Royal Mail has demonstrated that it can produce the cash flow demanded by its valuation with ease.

Normally we'd bite the hand off someone offering shares priced like this. But Royal Mail's position is more complicated.

The firm is really two businesses, UKPIL, UK Parcels International and Letters, the UK mail service,and GLS, General Logistics Systems, an international deliveries business. The latter makes money. The former doesn't, giving rise to distracting questions about whether the two belong together.

The firm has fallen out with its trade unions, and strike action has being threatened at various times in recent months.

The firm has fallen out with its Chief Executive. While it searches for a replacement, it is being run by a hastily appointed executive chairman.

The firm has fallen out with large investors, because it gave the departing Chief executive a bonus that they thought unearned and unnecessary. It has conducted an investor survey and introduced a new remuneration policy in an attempt to relieve this discontent.

Amazon, a significant customer, is turning into a competitor as it begins to undertake its own deliveries in some countries.

Most of all, though Covid has increased the number of parcels, UKPIL still relies for a lot of its revenue on letter deliveries, which have shrunk dramatically during the lockdown. The revenue splits 48% parcels and 52% letters. The 2020 accounts are dated 29 March but were not published until June, and so are able to include an indication of what April and May have looked like for UKPIL, with

parcel volumes growing by 37%

tracked products, ie parcels tracked and signed for on delivery, up 76%

addressed letter volumes down 33%

advertising mailings down 63%

business mailings down 19%

Taken together, these effects broadly cancel each other out, so that revenue is “broadly flat” compared with the equivalent portion of last year, but for one detail, which is that there was an election in the UK in May 2019, and Royal Mail was paid £29m to deliver communications from political parties, revenue that didn't recur in May 2020.

Delivering post in a pandemic is more expensive than in normal times, and the costs were "up £80 million, driven by overtime and agency resource costs due to high levels of absence, social distancing measures, protective equipment and parcel related volume costs."

Some simple extrapolation of these numbers will show UKPIL profits depressed by £509m in the current year compared with the last.

GLS is more modern, more international and focussed on parcels rather than letters. There, "B2B volumes have been adversely impacted; companies have scaled down their commercial activities. Conversely, we have seen a significant increase in B2C activity. Almost half of GLS’ volumes (48 per cent) are now accounted for by B2C; we expect that to grow to around 58 per cent by the end of 2020-21". The consequence is "Revenue up 15 per cent including acquisitions, driven by growth in B2C, and Operating profit margin improvement of 1.4 per cent."

Tiresomely, the effect on operating income for GLS is not quantified, but a profit reduction of £400m for the business as a whole would be the right order of expectation. The 2020 annual report shows two scenarios being considered by management which straddle this figure. [5]

A £400m fall in operating income would wipe out the 2020 profit before tax, which was £180m, so it is not surprising that the management has decided to stop paying dividends. However, a £400m fall would not wipe out the enterprise cash flow, which was £702m before we adjust it for items that can't be depended upon to recur, falling to £463m after we make those adjustments. This is consistent with the directors' conclusion that "Under both our stress test scenarios, our balance sheet and liquidity would be robust, with access to sufficient cash and unutilised facilities."

In fact, prudently or fortuitously, Royal Mail has already banked over £1000m of new debt financing before the pandemic gained momentum. €550m was a bond issued in October 2019, and £700m was drawn from a facility already in place from a syndicate of banks. It's not clear why these large amounts have been drawn as they are larger than needed by any plausible Covid scenario. At the end of March, these amounts were sitting in Royal Mail’s bank accounts.

Elsewhere, there is striking language in another context. Of the Universal Service Obligation, the duty that UKPIL has to serve every address in the United Kingdom, the board writes that it does

“not believe that the COVID-19 mitigation measures and the delivery of our transformation plan will be enough, in themselves, to ensure a sustainable future. We are also working with the Regulator and Government on a review of the USO. This is all about ensuring it is financially underpinned, in a sustainable way, and future-proofed to reflect changing customer needs and preferences."

Even in the context of the negotiation clearly under way with politicians and unions, we see it as a choice best described as courageous in the current climate, when many directors are laying awake at night wondering whether their businesses really do pass the going concern tests, to describe a large part of a business as unsustainable.

Not obviously implausible

So the questions become: given what we now know, are any of the coloured lines on the graph plausible extrapolations of the grey and black lines, which show Royal Mail's actual and adjusted historic cash flows? Not really. None of them drop far enough to reflect what is pretty inevitable in 2020.

But what if we shifted all the coloured lines one year to the right, and increase them by 10% to preserve our desired rate of return during a fallow 2020? The red line would be consistent with a future in which Royal Mail's enterprise cash flow is essentially zero during most of 2020, which is FYE 2021, and so neither raises nor lowers the business’s current debt levels; then recovers to around £200m in the following year, making its way back to current levels by 2026.

Is this future plausible? Pier Analysis's instinct is that it's not obviously implausible. Certainly, it's not as implausible as what we need to believe of the sky high tech stocks.

The judgement to be made is how to set off this maths against the lack of a CEO, the unions’ demands and the politics of the Universal Service Obligation. We'd rather look at other parcel delivery firms before settling on a view, and that is what we will do in the next newsletter.

What next?

A distinctive feature of Pier Review is that it provides the financial model that underpins each analysis. To receive the spreadsheet

if you have not done so already, subscribe to Pier Review by using the box below

click here to pre-populate a message in your usual email program requesting that the spreadsheet be sent to you

switch to your email program and click Send to despatch the request.

If you find this analysis interesting, you can sign up to have others like it delivered to your inbox several times a week.

Share Pier Review with interested friends.

Notes

[1] Except for the ones sent by businesses and paid for by means of a franking machine or equivalent arrangement.

[2] https://www.royalmailgroup.com/media/9973/royal-mail-plc-prospectus-2013.pdf

[3] In common with many businesses, Royal Mail's net debt has gone up a good deal since last year, which is an artefact of the way leases are accounted for. For consistency, either one should adjust the historic debt numbers to follow the new rules, or alter the latest debt figure so that it is consistent with its predecessors. We find it expedient to do neither; it will be sufficient for our purposes to take the figures as presented.

[4] Settings its target return to a high 10% pa and wanting it within a short period of just 15 years characterises the more conservative attitude of Pier Analysis compared with most brokers and, these days, many investors.

[5] The scenarios set out in Royal Mail’s 2020 accounts are interesting illustrations of the process all management teams are having to go through, to assess whether their businesses are going concerns.

Scenario 1 is "consistent with a lifting of the current COVID-19 lockdown restrictions from early July 2020, but with a GDP decline of 10 per cent in the 2020-21 reporting year, followed by a recovery thereafter"

Scenario 2 is "a severe, yet plausible, downside scenario that assumes a second wave of COVID-19 in the UK resulting in a further three-month lockdown during the autumn/winter in the UK, and a further deterioration in economic conditions impacting the UK and GLS".