A supermarket makes money by buying goods from suppliers and selling them to customers for more than it paid for them. [1] Not so at Costco. This chain, not well known outside the US, describes itself as being in the business of operating membership warehouses. While a supermarket will celebrate if it contrives to sell an item at a much higher than usual mark up, Costco would view any such occurrence as a mistake. It aims to offer prices scarcely higher than wholesale, and makes its money by charging membership fees. In the US, basic membership costs around $60 a year. Without this fee income Costco’s net margins are just 1.1%; with it, they reach 3.3%.[2]

The company is routinely studied in business schools as an encouragement to think laterally in the search for ways to reshape an industry. Don’t accept the established norms. Seek to confound the incumbents by overturning the assumptions on which have anchored themselves.

It's worth reading what Costco itself has to say on this business model. From the 2020 annual report:

We believe that the most important driver of our profitability is increasing net sales, particularly comparable sales growth. ... Comparable sales growth is achieved through increasing shopping frequency from new and existing members and the amount they spend on each visit (average ticket).

Our philosophy is to provide our members with quality goods and services at competitive prices. We do not focus in the short-term on maximizing prices charged, but instead seek to maintain what we believe is a perception among our members of our “pricing authority” on quality goods – consistently providing the most competitive values. Our investments in merchandise pricing may include reducing prices on merchandise to drive sales or meet competition and holding prices steady despite cost increases instead of passing the increases on to our members, all negatively impacting gross margin as a percentage of net sales (gross margin percentage).

Subjective impressions

In analysing Costco, a characteristic that stands out is the cleanness of the accounts. In our note on Tesco, we fretted about the presence within the company of a bank, perturbing the balance sheet and obscuring the cash flows. For Marks and Spencer, to be covered soon, we need to delve into two notes to the accounts before we can combine the income statement and the cash flow into the direct cash flow format favoured by Pier Analysis.[3] Both companies' accounts are riddled with exceptional items, discontinued operations and non-standard accounting metrics. Costco is entirely clear of this nonsense.

News channels are full of reports of retailers, wounded by the disappearance of some of their market online, and finally killed by the Covid-induced interruption to normal trade. What actually finishes off these businesses is a burden of debt that has developed over years to the point of unsustainability. While Costco does have $10b of debt, it has $12b of cash.

Costco has other benign characteristics. Its revenues are growing at 9% pa. That is not just the average growth rate over the last five years. It is also within a percent of the growth rate in every one of those years; the consistency is striking. Its financial year ends in August, so the last half of its 2020 was affected by Covid, but that was no obstacle to it delivering another year of 9% growth. Compare this performance with the large number of retailers that are shrinking.

Costco has operations outside the US, but they are growing no faster than its domestic ones. Not for it a sprint to foreign adventures that its competitors have spent recent years unwinding. [4]

Too many people would stop at this point, judging this company to be excellent and bursting to hold its stock. A company can have outstanding managers delivering world-beating products, but that does not make it an attractive investment. Popularity has caused some companies' share price to be bid up to levels that are disconnected from the income they have any chance of generating. We have seen this with Apple and Tesla, though we have to admit that that has not stopped their prices rising further since we wrote about them. Has a similar fate overtaken Costco? Let us have a look.

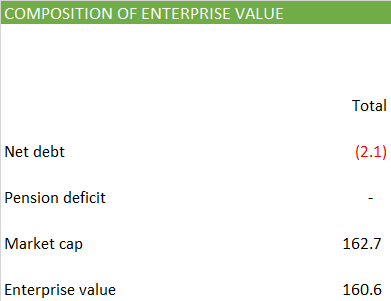

Enterprise value

As we have seen, Costco has negative net debt of $2b, the combination of $10b of debt and $12b of cash. We see this by picking out relevant entries from the balance sheet.

At today's share price of $367, the market value of Costco's equity stands at $163b. When we combine these figures, we find an enterprise value of $161b.

Required cash flow

Given this enterprise value, we can work out how large are the cash flows that Costco needs to be capable of generating for the value to be justified.

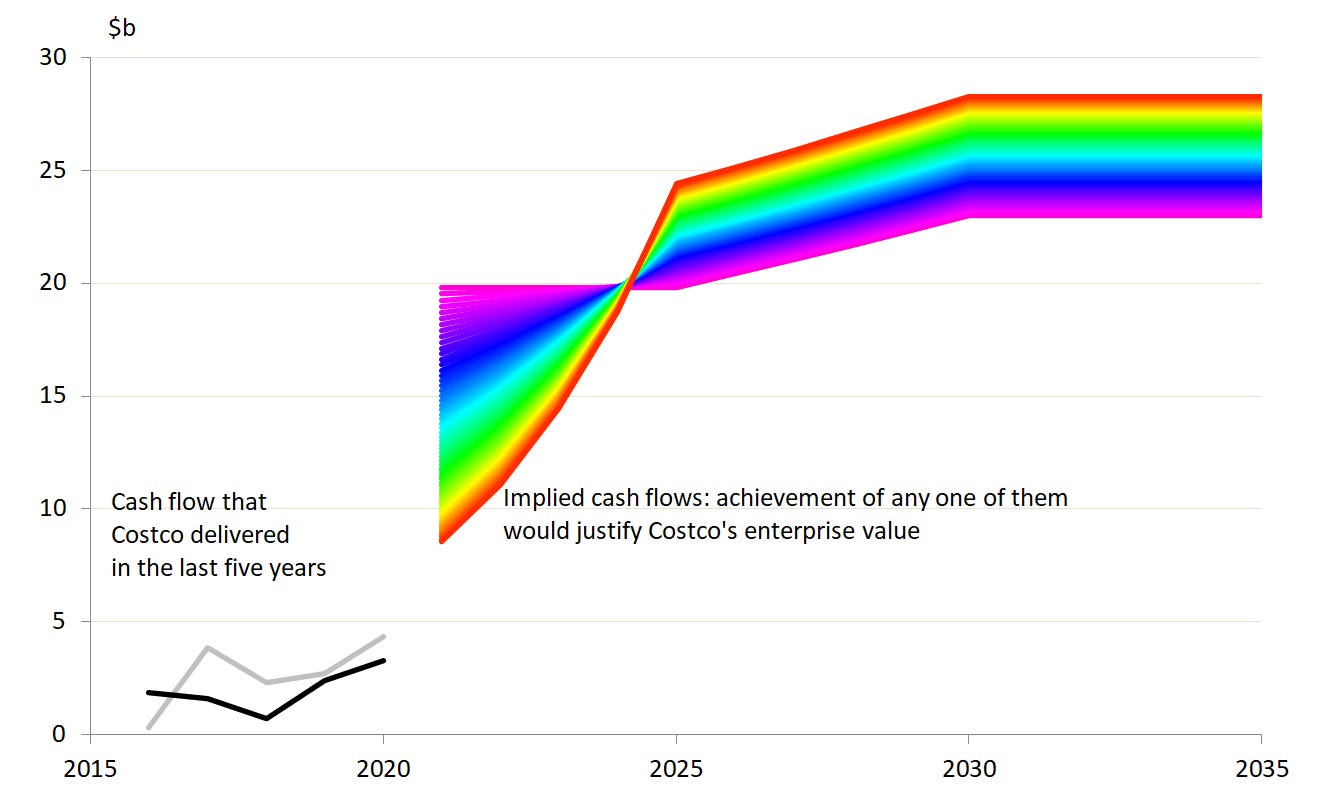

An investment in Costco would be justified if we could be confident that the company could generate $20b of cash flow, and that figure rose just a little over time to $23b. This is the violet line on the chart below.

Equally, an investment in Costco would be justified if the company could be relied upon to generate cash flow that started lower, at $9b, but rose more quickly to reach a higher plateau of $29b. This is the red line on the chart.

There are countless other possibilities between and beyond these extremes.

Actual cash flow

Now that we have an idea of the size of the cash flows that Costco needs to deliver to justify its valuation, we can compare that figure with what Costco has actually generated in recent years. Past performance is no guide to the future, but the comparison can identify companies where the required future is very different from what has gone before, and we can form a view of how plausible it is that that transformation might come about.

As is Pier Analysis standard practice, the cash flows have been re-expressed in a direct format, which is easy to understand. If you would like to see how these are derived from the much less intuitive indirect format favoured by accountants and presented in Costco's accounts, then:

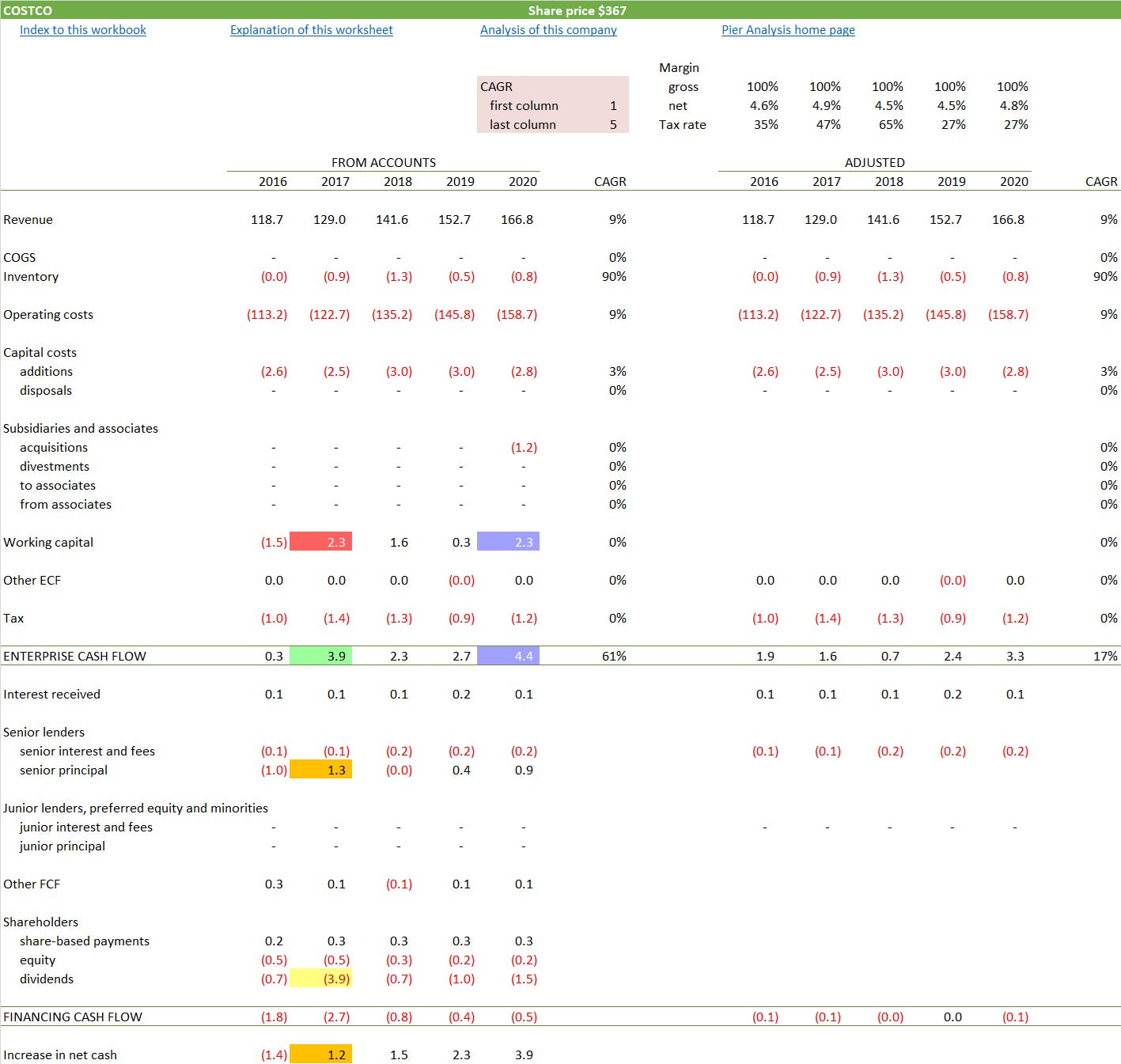

On the left of the direct cash flow are the numbers as so derived; on the right are the same numbers after they have been adjusted. The intention is to remove one-off items that are unlikely to recur, in pursuit of a sense of the underlying cash flows representative of what Costco might generate in the future.

Highlighted in green: Costco's revenues and costs are growing at 9% pa, as we've already observed.

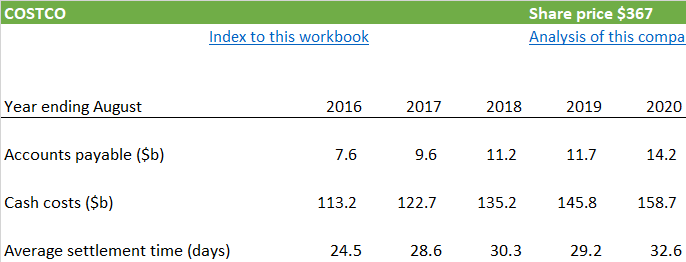

Highlighted in orange: Present in the historic numbers, but eliminated from the adjusted ones, are an acquisition in 2020, a rarity for Costco [4], and the benefits from working capital inflows. Like most supermarkets, Costco has sold its goods and collected payment from its customers, instantly in cash and not much slower by card, long before it has to pay its suppliers. Costco additionally has the advantage of collecting its membership fees at the start of the year. These combine to provide a favourable working capital cycle for as long as Costco is expanding. What is slightly more worrying is that this working capital benefit is at least partly due to Costco taking longer to make the supplier payments. It is about the only cloud we have noticed in the accounts.

Highlighted in grey and black: While we'd like to see cash flows of $10b and more, Costco's actual cash flow is of order $2-$4b. These are the quantities shown in the grey and black lines on the chart above.

Highlighted in purple: The growth rate of 61% pa is flattered by the benefit derived from working capital. Without it, it is closer to 17%.

Financing cash flow

Costco combines quarterly payments of dividends which rise at a cautious rate, around 8%, with intermittent special dividends. The last one was in 2017. To see how this came to be paid we look at the bottom of the direct cash flow, which concerns itself with financing.

Highlighted in yellow: The 2017 dividend is much larger than its neighbours because it included one of these special dividends.

Highlighted in orange: The firm drew down additional borrowings that year, not that it was necessary to pay the dividend. Most of the amount drawn was held as cash.

Highlighted in green: The dividend was financed out of cash flow, which was quite a bit higher than the previous year.

Highlighted in red: Much of the improvement in cash flow was due to working capital effects.

Highlighted in blue: 2020 joins 2017 in also having a noticeable boost to cash flow from working capital.

And, perhaps not coincidentally, Costco has announced another special dividend, to be paid in December and therefore falling into the 2021 financial year.

Verdict

The retail sector is a battlefield littered with well-publicised casualties. Battlefields are also populated by victors, and Costco's differentiated approach, consistent growth, apparent imperviousness to Covid, absence of debt and ability to pay special dividends mark it out as one.

Recognition of this case is now widespread, and amply reflected in the share price.

To justify its current valuation, one has to

allow Costco to return any investment in it over a period longer than the 15 year horizon that Pier Analysis favours; and / or

accept a rate of return lower than the 10% pa that Pier Analysis considers reasonable; and / or

believe that the company will break away from the prudent and purposeful practices that have characterised it and will make a dash for expansion at a rate closer to 40% than the 9% it has consistently pursued.

What next?

A distinctive feature of Pier Review is that it provides the financial model that underpins each analysis.

Many current valuations only make sense to those who are content with a return of less than 10%, and willing to wait more than 15 years for the return of their investment. If you are one of those, you can use the model to examine the effects of these less demanding requirements.

To receive the spreadsheet

if you have not done so already, subscribe to Pier Review by using the box below

click here to pre-populate a message in your usual email program requesting that the spreadsheet be sent to you

switch to your email program and click Send to despatch the request.

If you find this analysis interesting, you can sign up to have others like it delivered to your inbox several times a month.

Share Pier Review with interested friends.

Notes

[1] So you might think, but it's not the whole story. Most supermarkets rely for a surprising part of their profits on kickbacks from manufacturers for displaying their products in favourable parts of the store.

[2] Most of the time when Pier Analysis talks about margins it is contemplating the margins based on a company's cash costs, because Pier Analysis focuses on cash flows. Here, the margin being expressed is a more conventional margin based on the income statement.

[3] If a company is less than clear in its presentation of its cash flows to investors, it is open to wonder how the same information is being presented to its own management.

[4] The acquisition was of Innovel Solutions, which "provides final-mile delivery, installation and white-glove capabilities for big and bulky products across the United States and Puerto Rico". Costco has renamed it Costco Wholesale Logistics.

[5] For examples from 2020 alone, Walmart has sold the UK supermarket chain Asda which it bought in 1999. Tesco has sold its operation in Thailand.