It has long been a surprise that Vodafone is not a more successful company. It was there right at mobile telephony's start in the 1980s, gaining one of the first two licenses to operate a cellular network in the UK. The other was held by British Telecom which was hardly formidable as a competitor at the time. Vodafone expanded aggressively internationally, and at one point was the world's largest business in its sector. Most computing has moved from the desktop to users' handsets, and in the late 1990s it was widely accepted that the telecoms carriers were going to be able to capture a share of the value that would be created by that shift, with the result that Vodafone's share price reached a peak equivalent to over £5 in 2000.

Today the share price is a fifth of that. In the years before and after 2010, Vodafone was paying a dividend it couldn't afford, taking its debt to a level beyond which Pier Analysis judged any sane banker would let it rise further. The dividend payments were unsustainable and something would have to change, though it was not then obvious what that might be. This prediction proved accurate. Change came in 2013 in the form of the sale by Vodafone of its US operation, Verizon Wireless, to its partner Verizon, for $130b. Suddenly, the company was no longer highly indebted.

It's taken just six years for Vodafone to deplete that inheritance and restore its debt to levels verging on the uncomfortable. Its customer service makes BT's look good, and its market share continues to fall in most of the countries it covers.

Large among the culprits for the declining fortunes of telecoms companies has been the decision of governments to use spectrum auctions to transfer wealth from the companies' pockets to their own coffers. When continued future existence depends on gaining access to this scarce resource, it is hard for contestants to resist outbidding their competitors.

At this point much investment commentary would stop, dismissing Vodafone as a basket case. But it's possible for a company to be a bargain, even if it is not wonderfully successful, just as it is possible for wonderful businesses to attract valuations that are too high to make any sense. Is Vodafone one of these? We will take a look.

Enterprise value

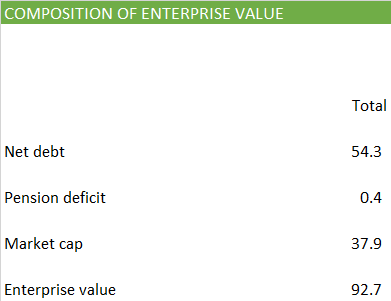

Study of Vodafone's balance sheet shows that it has €75b of debt, offset by €20b of cash. It also has a deficit of €0.4b on its pension scheme. This is a surprise. British Telecom, which we studied in our previous article, has a pension deficit, but it was demerged from the UK Post Office which is hundreds of years old. Vodafone is much younger and one might have imagined that it would be free of such historical encumbrances, just as most technology firms are, but no.

To find out the total enterprise value of this business, we need to combine these figures with the market capitalisation implied by today's share price of £1.2752.

Necessary cash flow

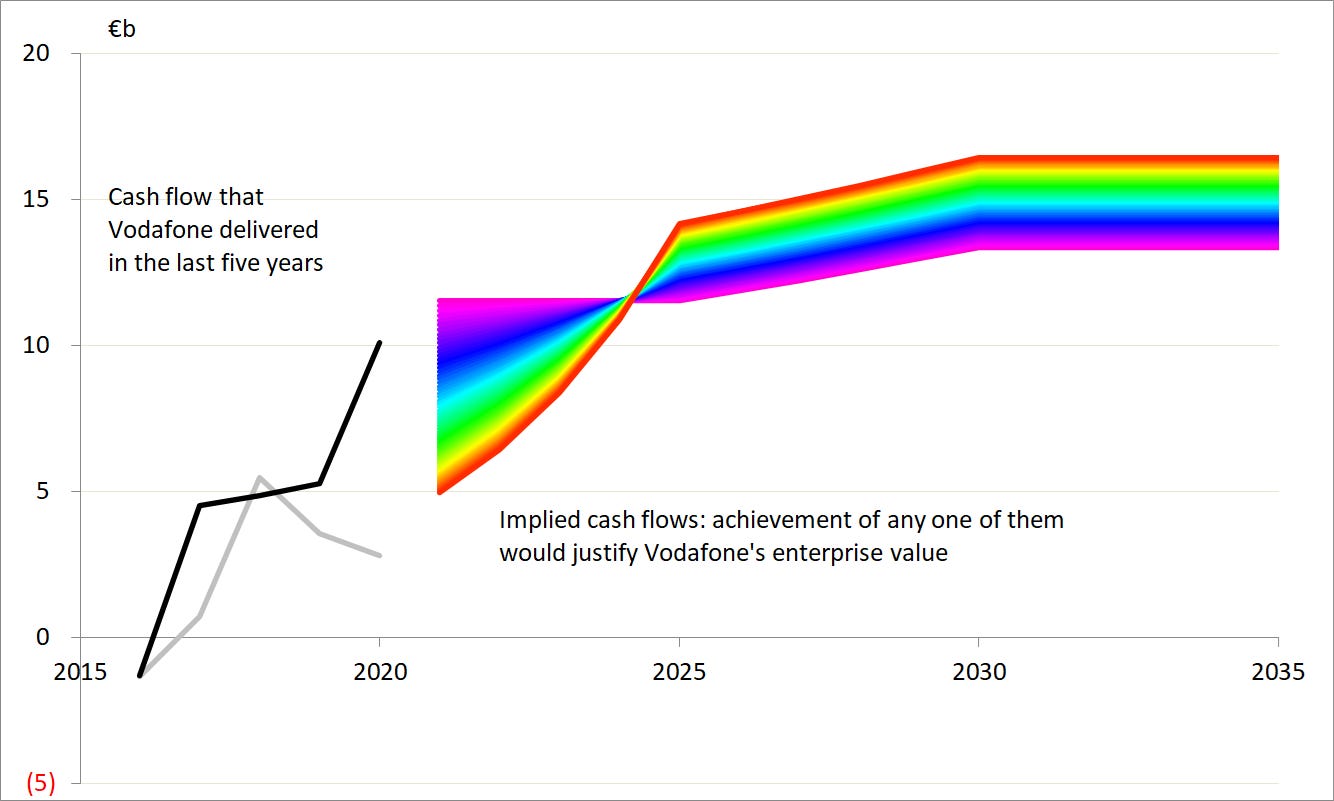

Once we know its enterprise value, we can work out how large are the cash flows Vodafone needs to generate to justify that value [1].

One way is to deliver cash flows around €11b to €13b: this is the violet line on the graph below.

Another way is to accept a cash flow that is lower than this range in the early years, say €5b, but makes up for that by growing rapidly so that it is significantly higher in the later years, reaching €16b. This is the red line on the graph.

And there are infinitely many contours between these two examples, and beyond them. If the cash flows that Vodafone generates in the future follow any of these lines, the benefits of holding a stake in the company (our entitlement to our share of these cash flows, discounted back to today) match the cost of buying that stake.

Actual cash flow

Now that we know how large cash flows need to be in the near future for an investment in Vodafone to make sense, we can see whether it is at all likely that Vodafone can deliver them by comparing them with what Vodafone has achieved in the recent past. As cannot be repeated too often, past performance is no guide to the future, but it is a help in identifying investment cases that demand implausible upticks in profitability.

The grey line shows what the accounts report: cash flow in the £0-5m range. The black line shows what the cash flow would be if adjusted to remove items that are unlikely to recur. Without those costs, Vodafone's cash flow is rising consistently from below zero in 2016 to above €10b now.

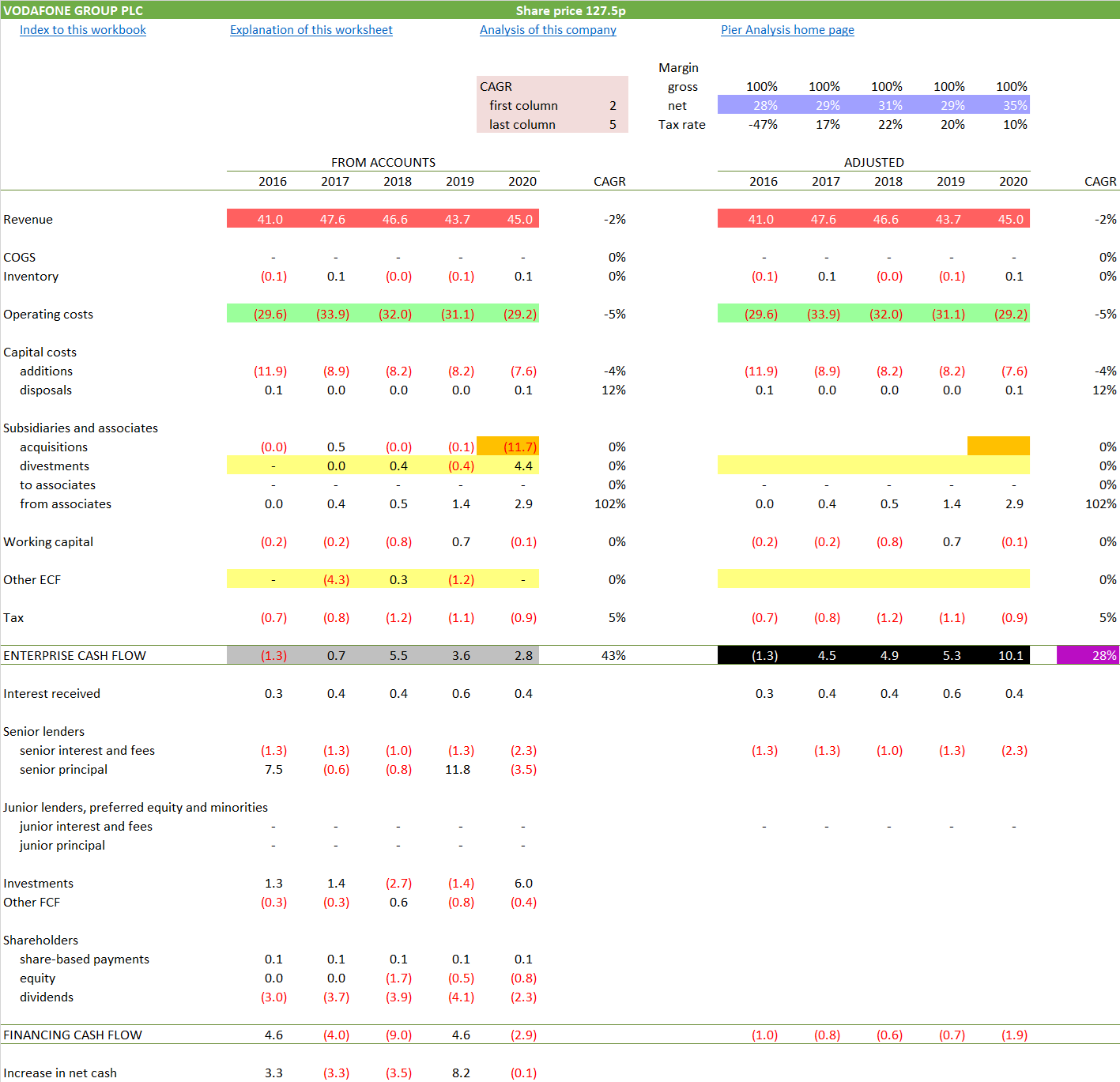

These black and grey profiles are taken from an analysis of Vodafone's cash flow.

Highlighted in grey: Vodafone's enterprise cash flow as inferred from the accounts.

Highlighted in black: Vodafone's enterprise cash flow after making adjustments to eliminate non-recurring items, in pursuit of a sense of the firm's underlying cash flow.

These are the profiles shown in grey and black on the chart.

Highlighted in orange: The chief adjustment is the removal of the cost of acquiring the European assets of Liberty Global in 2019 [2].

Highlighted in yellow: Also removed are the proceeds of divestments, and the cash flow from discontinued operations.

Highlighted in red: Vodafone's revenues are shrinking. This is surprising. It is explicable in Western markets, which are mature; but Vodafone trumpets its international reach, and covers markets such as India which one might expect still to be growing.

Highlighted in green: Vodafone is making good progress in controlling its cash costs.

Highlighted in blue: As a result, Vodafone's cash margins are improving.

Highlighted in purple: The upshot is that Vodafone's cash flow has been growing at 28% pa over the last four years. (2016 is excluded in this calculation as the figure then was negative).

Vodafone's enterprise cash flow is on a rising trend and, if we believe that the €10b of cash flow that it generated after adjustments is the new standard level for the firm, we can see that it is already achieving most of what it needs to achieve to justify its current valuation.

Financing

In our last newsletter we found that BT, too, showed a promising trend in its enterprise cash flow, but that it was hard to rationalise management's decisions when it came to the financing cash flow. Much the same is true of Vodafone.

The illustration below shows the key elements of Vodafone's financing in the five years ending 2016-2020.

Highlighted in light blue: The firm spent €11b acquiring Liberty Global

Highlighted in red: It raised the means to pay for Liberty by issuing a bond. This gave rise to a sharp downgrade in the rating allocated to Vodafone's debt by agencies such as Moody and Fitch.

The very best companies such as Apple and Alphabet can buy pretty much any business they want with cash they already have on hand. More ordinary enterprises have to borrow. Borrowing to make a major investment is not wrong, but the expectation is that past borrowings will in due course be paid back. What is troubling is that the size of the amounts borrowed were larger than the acquisition costs, showing that Vodafone has not been successful in paying down past borrowings. The reason is that Vodafone has, yet again, been paying dividends that, along with the interest cost of all that debt, and a share buy back programme that it has, inexplicably, been pursuing, amounts to more than the cash that it has been generating.

Vodafone has yet again been paying dividends beyond what it can afford, and borrowed to do that and pursue acquisition adventures that have taken it back to the position it was in earlier in the decade.[3]

What is the modern equivalent of a divestment of Verizon? We find it in two forms.

The first is a cut in the dividend, which is an acknowledgement at last of the problem.

From the 2019 annual report:

Rebasing the dividend to support Vodafone’s transformation and rebuild headroom

Vodafone is at a key point of transformation – deepening customer engagement, accelerating digital transformation, radically simplifying our operations, generating better returns from our infrastructure assets and continuing to optimise our portfolio. In order to support these goals and to rebuild headroom, the Board has made the decision to rebase the dividend to 9 eurocents per share. This will help us to reduce debt and move to the lower end of our targeted 2.5x-3.0x leverage range in the next few years.

The second is an IPO as a separate business of its cellular transmitters, to be called Vantage Towers.

News reports suggest that the IPO will raise €4.5-6b, though the final pricing is yet to be determined.

The IPO will have several effects.

It will patch up the ragged balance sheet, a bit, though €5b from the IPO is modest compared with the €54b of net debt.

It will trade capital expenditure for operating costs, since investments in cell towers that Vodafone makes now and which show as capital expenditure in its accounts will become costs for Vantage Towers. In exchange for that, Vodafone will have to pay some kind of access charge, which will serve as a cost for it but as revenue for Vantage. Vodafone's capital costs have averaged 20% of revenue over the last five years, and would likely rise due to the rollout of 5G and beyond, a problem it will now be relieved of. Our guess is that the costs of acquiring new spectrum for 5G and future technologies will continue to be for Vodafone's account, but the capital costs outside this category will be split roughly evenly between tower infrastructure, which will move to Vantage, and central network switching systems and customer facing activities such as shops and billing, which will not. Those costs that do migrate will in effect be amortised over a much longer period than Vodafone can borrow over at the moment.

Like any demerger, the IPO may unlock value as investors come to understand the attractions of the businesses more clearly when they are separated.

Pier Analysis's own background is in the financing of infrastructure, and practitioners in that field have long been arguing that telecoms companies should not struggle under the weight of the investment required to roll out the 5G network. They should be delegating those costs to specialist vehicles away from their balance sheet. In this way they could gain access to the long term financing available to infrastructure assets. The engineering cultures in these organisations have made them reluctant to follow this suggestion. Now at last we see the major protagonists in the industry moving down this path. If BT sees its rival managing this transition successfully, it may be tempted to copy the plan itself, which could unlock value in that company too.

Verdict

Taking these things together, we have a business which has

an enterprise cash flow that is improving, and is already close to what it needs to be to rationalise the current valuation

the tower transaction which will further improve the cash flow

financing practices which are hard to admire, leading to a sorry looking balance sheet and an only just prime debt rating, but which will also be improved by the proceeds of the IPO.

Against these things, we find a business that is inescapably at the mercy of governments’ spectrum auctions, and which can't seem to reverse the erosion in its top line, no matter how much it invests and acquires, and even though it is active in markets such as India and Africa which one might have imagined to be fast growing.

The question comes down to whether the improving cash flows and the tower IPO mark a permanent break from the uninspiring past. At the current appealingly low valuation, we would be inclined to make that bet, though we do so mindful that CEO Nick Reid, in post since 2018, was in charge of finance between 2014 and 2018.

What next?

A distinctive feature of Pier Review is that it provides the financial model that underpins each analysis.

Current technology valuations only make sense to those who are content with a return of less than 10%, and willing to wait more than 15 years for the return of their investment. If you are one of those, you can use the model to examine the effects of these less demanding requirements. You will see the coloured lines on the graph, which show the projection of cash flow required to justify the valuation, will shift downwards. (The black lines on the chart will not move, since they are the result of Vodafone’s reported historic performance.)

To receive the spreadsheet

if you have not done so already, subscribe to Pier Review by using the box below

click here to pre-populate a message in your usual email program requesting that the spreadsheet be sent to you

switch to your email program and click Send to despatch the request.

If you find this analysis interesting, you can sign up to have others like it delivered to your inbox several times a month.

Share Pier Review with interested friends.

Notes

[1] Pier Analysis takes the view that a viable destination for cash available for investment is any of many funds that specialise in owning infrastructure assets such as hospitals, schools, power stations and renewable assets. These assets often exhibit very dependable cash flows as a result of having national and local governments as their customers. They typically have lives of 30 years, and the average asset held by a fund will be halfway through this life and so have fifteen years to go. The returns promised by these funds when they launch is typically in the range of 8-11%. Pier Analysis therefore seeks to match this alternative by seeking a return of 10% pa and requiring it to be delivered over a fifteen year period.

[2] Stripping out acquisitions in this way has to be done with care. The argument for removing them is that the company now owns what it has acquired and does not need to make further payments in future years to continue to benefit from what it has bought. The case in the opposite direction is that we are in danger of including the benefits of acquisitions, by including its effect on revenues and margins, but ignoring the cost of gaining that increase, by stripping out the acquisition cost. It is easier to rationalise the removal of acquisitions in companies that make them infrequently than in companies that make them repeatedly and depend on them to fuel their growth trajectory.

[3] It is interesting to speculate about why this might be. Pier Analysis believes strongly that most companies present their cash flows in a way that is hard to follow. Pier Analysis goes to significant effort to show cash flows directly, starting with a business's revenues and stripping away successive layers of costs. Accountants favour an indirect approach, where cash flow is calculated by adjusting numbers laid out in the income statement. The result is that the basic drivers of cash flow, the company's revenue and costs, are nowhere to be found on the cash flow statement, and the reader has to flip between the two statements to understand the connection between the top line and the bottom one in cash terms.

In Vodafone's case, the position is worse than usual. The detail needed to understand the cash flow is spread out over not just the income statement and the cash flow statement, but a crucial portion of it is buried in note 18 or 19 to the accounts. All three of these elements need to be brought together to see the overall picture.

This leads us to wonder what information the Vodafone board is receiving so far as concerns the relationship between the dividends they are responsible for proposing and the cash generative performance of their company.