More in our series investigating the possibility that businesses delivering parcels will benefit from higher volumes as individuals confined to working from home order more items online.

This time we stumble on a company that really does fall into this category. UPS depends on Amazon for over 11.6% of its revenue, and its share price has shot up by 60% since the depths of the pandemic-induced uncertainty.

Enterprise value

Study of UPS's balance sheet shows that it has $28b of debt, offset by $6b of cash. It also has a deficit of $11b on its pension scheme. To find out the total enterprise value of this business, we need to combine these figures with the market capitalisation implied by today's share price of $160.3.

Determining the market capitalisation is a little less straightforward than usual, as UPS has a special class of share reserved for employees.

We maintain two classes of common stock, which are distinguished from each other by their respective voting rights. Class A shares of UPS are entitled to 10 votes per share, whereas class B shares are entitled to one vote per share. Class A shares are primarily held by UPS employees and retirees, as well as trusts and descendants of the Company’s founders, and these shares are fully convertible into class B shares at any time. Class B shares are publicly traded on the New York Stock Exchange ("NYSE") under the symbol “UPS”.

Since the Class A shares are convertible into Class B shares and share in any dividends UPS chooses to pay out, the two classes need to be combined to work out the company's market capitalisation. Most online sources show the capitalisation of the B shares only and so underestimate how much this business needs to achieve to justify a given share price.

Taking all this into account, we come up with an enterprise value for UPS of $170b.

Necessary cash flow

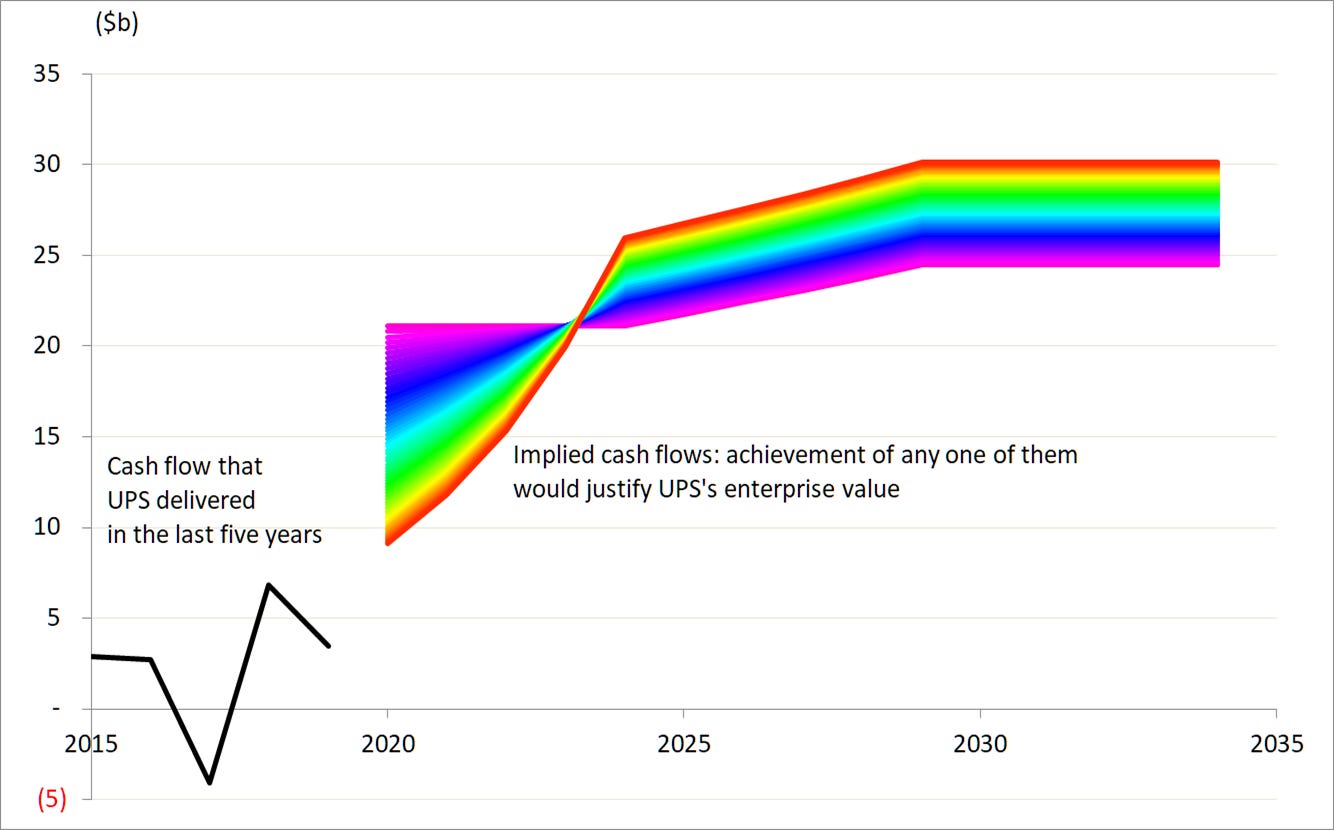

Once we have a handle on the enterprise value, we can work out how much cash flow UPS needs to generate in order to justify this valuation. [1]

Among the range of trajectories that would do the job is one that starts around $21b and rises gently to $24b: this is the violet line on the graph below.

Another way is to accept a cash flow that is lower than this range in the early years, say $9b, but makes up for that by growing rapidly so that it is significantly higher in the later years, reaching $30b. This is the red line on the graph.

And there are infinitely many contours between these two examples, and beyond them.

Actual cash flow

Now that we know what UPS needs to achieve to reward us appropriately and return our capital to us, we can look to see what the company has actually managed. The black line at the left in the graph above shows what UPS’s enterprise cash flow looked like in the last five years.

Most years, UPS has generated $3b - $7b.

Our instinct is that the chance of these cash flows rising to $21b and beyond any time soon is negligible, no matter how many Amazon parcels the firm gets to deliver.

Spending money it hasn’t got

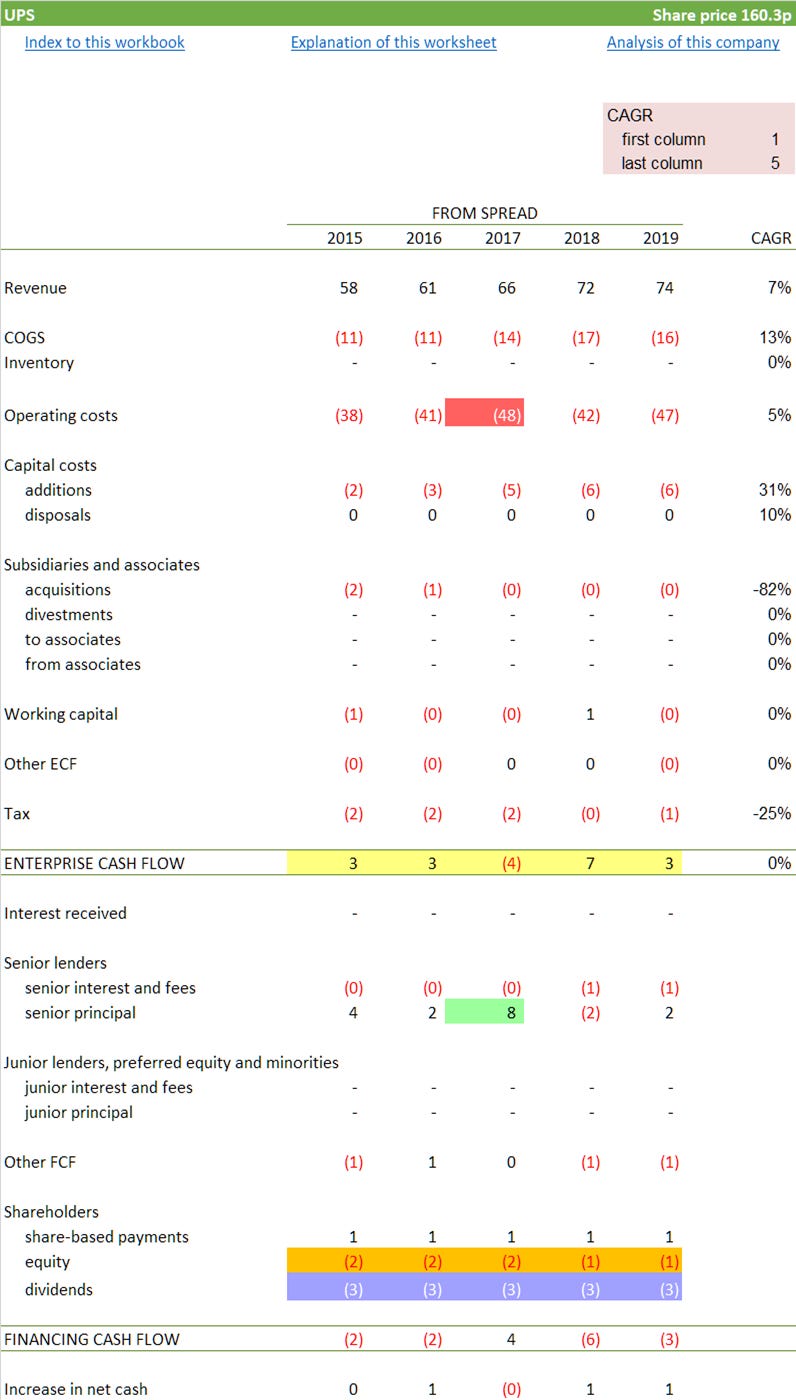

Pier Analysis goes to considerable trouble to recast the cash flows of businesses that it examines into a direct presentation. It is much easier to see what is going on in this layout than it is in the indirect presentations favoured by accountants and offered in published accounts.

Doing this to UPS's historic cash flows makes visible a couple of interesting features. Though most years it generates $3-7b of enterprise cash flow [highlighted yellow in the exhibit below] in 2017 the cash flow was sharply negative, the result of a sharp rise in costs [highlighted red]. That was the result of making a substantial payment into the pension scheme. It was necessary to borrow to cover this cost [highlighted green].

But the borrowing doesn't stop there. It's been a feature of four of the five years up to 2019. The result has been for UPS's net debt to double over that period.

Even so, the company has continued to pay dividends [highlighted blue], and continued its pursuit of a share repurchase programme [highlighted orange].

Pier Analysis seeks to apply to the evaluation of well-known companies the distinctive outlook of professional investors in infrastructure, and a company specialising in this class of asset wouldn't dream of paying dividends out of money it hasn't got. Still less would it use borrowed money to buy back its own shares. The contracts that governed it would simply disallow any such thought.

These constraints are peculiar to the world of infrastructure. Outside it, companies can and do borrow to pay dividends, but it is normally an occasional practice applied only in years of cash tightness, when there is a clear path to better times in future. As for share buybacks, they are appropriate for companies that have more money than they know what to do with, Apple being the obvious example.

A company will eventually run out of borrowing capacity if it draws down additional debt every year. In some cases, companies aim to maintain a constant level of gearing, which means that they borrow more as they get bigger, the debt growing a little each year but remaining more or less constant relative to the increasing size of the company. But that isn't what is happening here. As a portion of UPS's revenue, its debt has risen from around 24% to 34% in just five years.

Metrics of its own devising

Another unattractive behaviour pursued by UPS's management is to devote pages of its report to measures of its own devising, which are non standard and don't conform with generally accepted accounting principles. Like Royal Mail, UPS is engaged in what it calls transformation, a word that appears 58 times in the 2019 report, yet its adjusted metrics carefully strip out the cost of this transformation. As we've seen with the other delivery companies we have studied in recent weeks, transformation is a constant in this industry and not something that can be dismissed as exceptional and temporary.

In the search for motivations for both policies, UPS's LTIP, that is, its long term incentive plan, rewards study. Members of the plan are incentivised by the prospect of “Awards” that are linked to

the adjusted measures of profit and cash just described, the effect of which are to remove much of the incentive for restructuring and transformation to be pursued economically

dividends paid on a per share basis, which incentivises high dividend payouts and buy backs to reduce the number of shares

total shareholder return, measured mainly through stock price appreciation, which again is flattered if the business can reduce the number of shares in issue through buybacks.

Tilted playing field

In recent years as much as 60% of the resources used for the buy back have been directed at the A shares, even though they are just 19% of the total shares outstanding.

Remind us who holds the A shares? This is where we came in in this article.

Class A shares are primarily held by UPS employees and retirees, as well as trusts and descendants of the Company’s founders

The likelihood of any of this changing is not high while

Class A shares of UPS are entitled to 10 votes per share, whereas class B shares are entitled to one vote per share.

In other words, current and past employees have 69% of the votes in UPS.

Counterarguments

While UPS’s debt has doubled in five years, most of the increase was the result of UPS making a substantial payment into its pension fund in 2017. Compared with this big one, the deficits in other years are modest.

Arguably, UPS substituted one liability, pension deficit, for another, higher debt, and is no worse off than it was. The position of the A share holders, as employees, is of course considerably improved.

The rating agencies have a more positive outlook than this note. Though Standard and Poor’s and Moody's downgraded UPS a year ago, it was from A+ to A, showing that they have no doubts that the business can sustain its current levels of borrowing. Not every conclusion that these agencies arrived at over the last ten or fifteen years has turned out to be perfectly founded.

While it’s true that external shareholders in UPS can be outvoted by the internal shareholders, their position is better than some of the tech firms. There the outsiders get no votes at all, but it doesn’t stop these firms commanding some very fancy valuations.

Not hard

When we combine management choices, in the form of uncovered dividend payments and share buybacks, an unhealthy looking LTIP, a minority voting position for outside shareholders, and a valuation that lacks any solid grounding in the cash flows, it is not hard to move on from UPS in one's search for interesting opportunities.

What next?

A distinctive feature of Pier Review is that it provides the financial model that underpins each analysis. To receive the spreadsheet

if you have not done so already, subscribe to Pier Review by using the box below

click here to pre-populate a message in your usual email program requesting that the spreadsheet be sent to you

switch to your email program and click Send to despatch the request.

If you find this analysis interesting, you can sign up to have others like it delivered to your inbox several times a week.

Share Pier Review with interested friends.

Notes

[1] By justifying the valuation, we mean we require UPS to be able to generate future cash flows that have a present value equal to its $170b enterprise value, when discounted at 10% pa over 15 years. Any one of the cash flow profiles discussed would put UPS in the position to return our investment within 15 years and give us a 10% return while we wait for it.