Thomas Pink

How to lose your shirt to the tune of £100m

News reports of the closure of London retailer Thomas Pink attribute its demise to the pandemic. No one needs to buy the kind of shirts it sells when they are not going to the office. That explanation is less than half of the story, and the rest of the story contains several interesting lessons.

Thomas Pink is a chain of shops, mostly small, mostly in London, that sell shirts. Ties too, and similar things; but mainly shirts.

It differs from the well-known businesses that have featured in Pier Review in that

it is hardly international: only a few of its outlets are outside the UK

it is not significant: its revenue is no more than £12m, which is around $15m

it is not quoted on any stock exchange.

And it differs from them in that it has ceased to trade. The shops are boarded up and for some time the web address served up no response to queries. Now it delivers a holding page promising some form of resurrection for the business.

It is not unusual for shops to close down. Plenty of high street retailers are in difficulty. We examined one in our coverage of Marks & Spencer. Covid has made things worse, by keeping people out of entire districts where Pink's stores are located (that includes airports, where Pink has several outlets), and confined to their homes, where buying shirts is neither a priority nor even a necessity.

But Pink’s closure is interesting because the team at Pier Analysis likes its shirts, and mourns its loss; and because its accounts make extraordinary reading.

Cumulatively, it has lost nearly £100m.

In 2019 alone, it reported losses four times larger than its revenue.

Even so, it chose to pay its three directors close to £4m.

Its numbers give rise to reflections about the configuration of complex companies, including Thomas Pink’s owner, a collection of some of the most famous brands in the world: Moet Hennessy Louis Vuitton SA, better known simply as LVMH. And that definitely is quoted, international, and significant.

Background

Those who want expensively hand-made suits in London go to Savile Row, a street where tailors have congregated since the early 1800s. Less well known is that there is another street nearby, Jermyn Street, which is equally specialised in the sale of shirts. Expensive ones.

In the late 1980s three brothers set up Thomas Pink to sell similar shirts at more affordable prices, something that they achieved at least in part by locating their first shop in a residential part of London well away from Jermyn Street. It did well. Within not much more than a decade LVMH bought 70% of the business for about €48m, and took the remaining 30% in 2003.

Cash flow

All stock exchanges require companies which list shares on them to publish accounts at least annually. In most countries, companies that are not listed, which are the great majority of businesses, are under no obligation to disclose their numbers. In the UK, it's different. Every company must file accounts with an agency of government, where they are available for public inspection. The ones for Pink can be found here https://find-and-update.company-information.service.gov.uk/company/01995666/filing-history.

Most company accounts set out their financial results in terms of an income statement, a balance sheet and a cash flow. Pier Analysis concentrates on the cash flow and rearranges it so that it is much easier to understand than the opaque layout provided by the accounting profession. Thomas Pink is small enough not to have to publish its cash flow, so Pier Analysis has had to do more than rearrange the numbers provided. It has had to work out what they must have looked like by inferring the position from the income statement and the movements in balance sheet from one year to the next. They won’t be perfect [1], but the resulting reverse engineered cash flows are close enough to give us a good idea of Thomas Pink's unusual numbers.

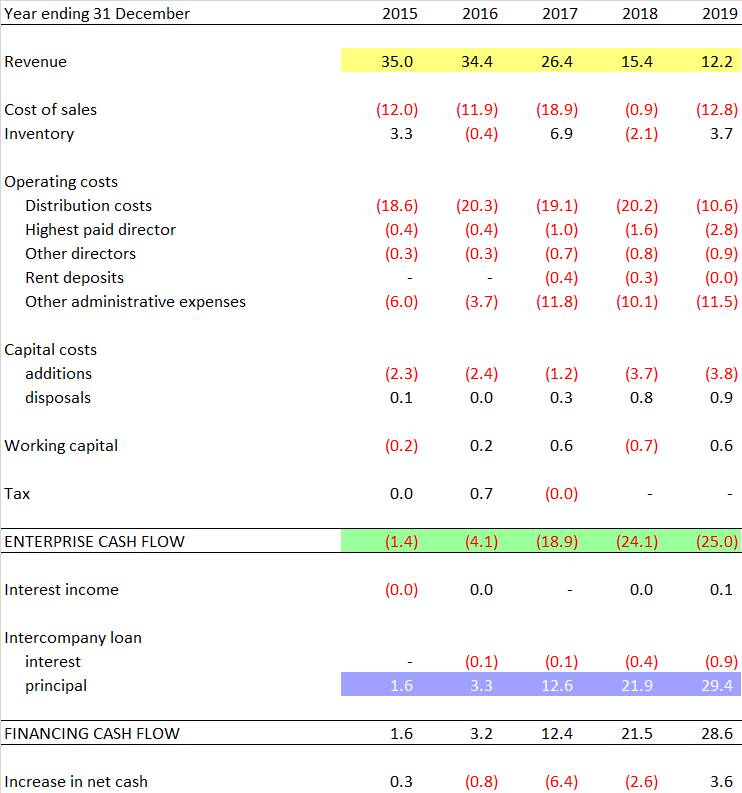

Click this exhibit to make it larger and easier to read.

Highlighted in yellow: Thomas Pink’s sales in 2019 were a third of what they were in 2015.

Highlighted in green: As a result of the sales collapse, the company started haemorrhaging cash; over £70m in the period shown.

Highlighted in blue: The company borrowed increasing amounts from its parent company to stay afloat.

This cash-flow perspective makes the position look less bad than conventional profit-based measures, which record cumulative losses of closer to £100m as a result of writing down past investments. And these figures don't yet include 2020, which is unlikely to have improved the position.

Why did sales collapse?

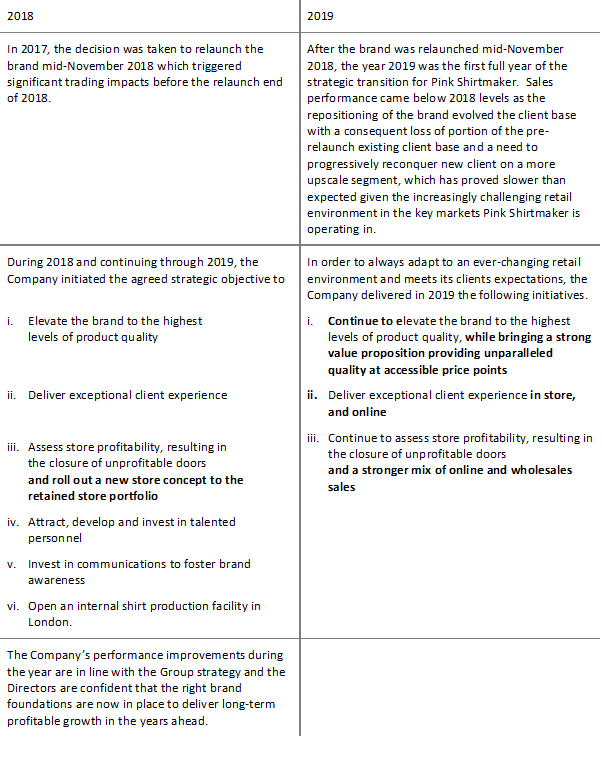

The fall in sales dates back to 2015 and was well on the way in 2017. That’s long before Covid was even a word. The company described what was going on in its annual reports. Putting extracts from 2015, 2016 and 2017 side by side makes plain an enthusiasm for copying and pasting. Looking at where the narrative changes from one year to the next shows the approach beginning to shift.

Click this exhibit to make it larger and easier to read.

The tone changed in 2018 and 2019.

What unfolded here is not a haphazard strategic mis-step in a shirt retailer. Rather, it is a complete failure of the playbook that is shared by all international luxury brand businesses. They expect to pick up a product with some regional profile, professionalise its management and branding, push it up market in terms of product quality and price, and present it to a new audience that is wealthier and more international. In Thomas Pink, this plan led not to enlargement but to shrivelling. It is open to ask how many other expensively acquired luxury marques are similarly resistant to the brand houses’ formula.

Costs

What was happening to Thomas Pink’s costs while its revenues were collapsing? Before answering that, it’s worth asking what its costs consist of. Thomas Pink divides them into three categories,

Cost of sales: the cost of buying the shirts from manufacturers

Distribution costs, which no doubt covers rent and staffing costs for the retail outlets and warehouses

Administrative costs: costs of head office, web site and other central costs.

Under the ownership of a conglomerate like LVMH, Thomas Pink probably has another cost to add to the list. It’s likely that LVMH charges some kind of franchise fee, through which it recovers the costs of providing its managerial beneficence.

In the short run, large companies can help themselves to any cash their acquisitions generate. As Thomas Pink’s 2019 annual report records

The Company is part of the LVMH Group, which operates under an “Automatic Short-Term Cash-Pooling System”, whereby various companies within the LVMH Group pool their cash operations in order to rationalise the management o f available funds and financial requirements.

As the last two words in that extract allow, in the case of a loss-making subsidiary such as Thomas Pink, the flow of cash is reversed: the central pooling arrangement supplies to the subsidiary the cash that it needs to stay afloat. But that doesn’t alter the point that all LVMH’s businesses are under the management of a common treasury operation, their cash positions thoroughly mingled.

In the long run, however, a parent company can’t help itself to a subsidiary’s money. The subsidiary has directors who are subject to legal obligations to look after their company’s assets just as if the company was owned by independent shareholders. They can’t hand property of the company to an outside entity because it happens to have become the owner. If cash is to be passed up, it has to be done in the form of dividends, declared by the subsidiary’s directors according to the rules that apply to everyone; or lent, in the form of intercompany loans that will be well documented and faithfully accounted for.

Or, there’s another way. Parent and subsidiary can execute some kind of agreement by which the latter pays the former a fee for the services provided by the central function. The fee might be a fixed annual amount, or a percentage of revenue. It is a much better mechanism for extracting cash from a subsidiary than dividends: the fee can be set off against tax within the subsidiary (it will be taxed as income in the parent, but the parent can be located somewhere where tax rates are not too burdensome); it is not limited to how much profit the business makes; and it can be charged continuously rather than just once or twice a year.

Thomas Pink’s accounts are hardly forthcoming on these arrangements, but they do hint at them in various notes to the accounts.

Note 2: As permitted by FRS 101, the Company has taken advantage of the disclosure exemptions available under that standard in relation to … related party transactions.

Notes 17 and 18: Amounts due from / to group undertakings are unsecured, interest free and are repaid in accordance with the terms specified in the governing distribution agreements.

Note 22 to the 2015 accounts: Related party transactions The Company is exempt per paragraph 8 (j) and (k) of FRS101 from disclosure of transactions with other group undertakings where 100% of the voting rights are held within the group.

Though the accounts withhold the information that would show how large they might be, it is reasonable to conjecture that Thomas Pink’s costs include payments to its parent. Such payments allow recovery of the cost of services provided by LVMH’s head office, such as but not limited to that central treasury function, and provide a convenient mechanism for passing cash to the parent free of the norms that constrain dividend payments. If the payments were very large, they alone would be enough to drive Thomas Pink into its loss making position.

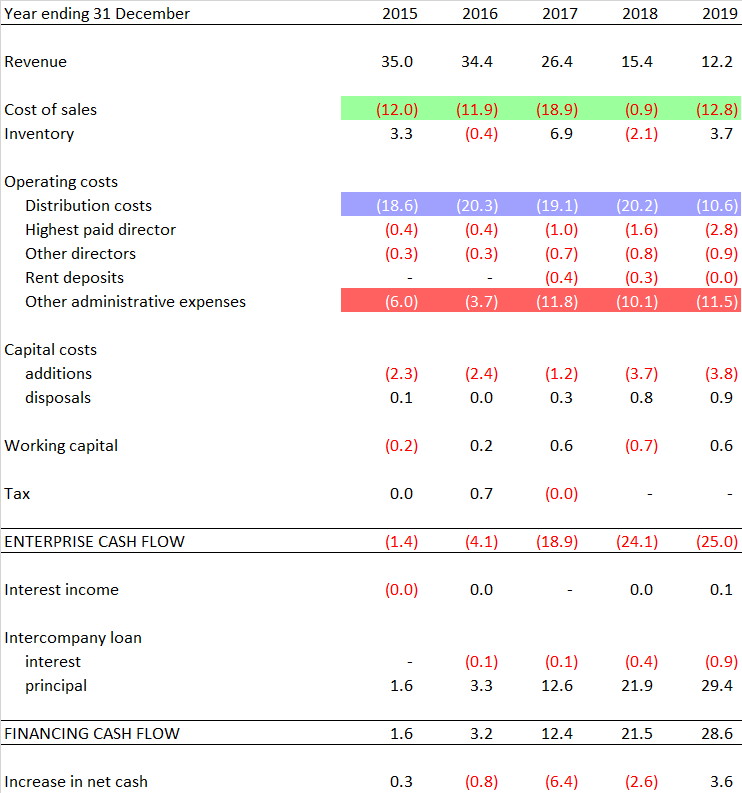

This is the context to be born in mind when we see how the costs of Thomas Pink behaved as the revenues shrank.

Highlighted in green: The cost of the shirts themselves will be captured by the cost of sales line.

Highlighted in blue: Is £20m a year a reasonable cost for the rent and payroll costs of the shops and warehouses?

Highlighted in red: Is £10m a year a reasonable cost for administrative costs, which presumably covers the head office, accounting, HR, IT and the website?

Keep in mind in answering these questions that this is a business turning over £25m and falling, with no more than a dozen outlets [2], some of them very small, in for example train stations. [3]

The extent to which any of these costs seem higher than one might have expected could be an indication that they have been enlarged by service, licensing, franchise or distribution agreements with the parent company.

Directors’ remuneration

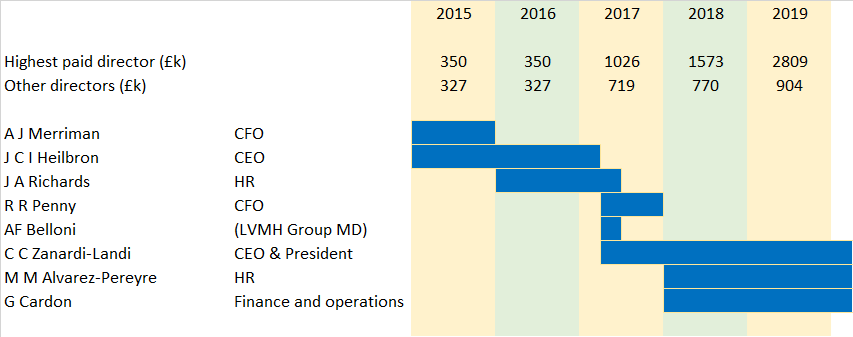

The administrative costs highlighted in red are lower than suggested by the accounts because we have peeled out of them the amounts paid to Thomas Pink’s directors, since we show them separately in our cash flow. They have more than quadrupled between 2015 and 2019. In 2019, for every £120 spent by a customer on a shirt or two, £37 went to the directors. £28 went to one director alone, who received £2.8m for the year as a whole. This is a decent reward under any conditions, and becomes particularly intrepid in a business whose cash losses are twice as large as its sales.

The accounts don’t say who the highest paid director is, or even if it is the same individual in every year. To see who it might be, we can compare the arrivals and departures from the board with the pattern of payroll costs.

We’ve been racking our brains to think of circumstances under which well advised directors of a business could sanction payments on this scale at a time when the company was haemorrhaging cash faster than it was earning revenue. About the only arrangement that we can think of is that the parent willingly formalised an agreement which compensated Thomas Pink for doing so, as an element of a carefully formulated group-wide remuneration structure for the individuals concerned.

LVMH is huge

We have made no detailed analysis of LVMH, though we intend to do so. A casual reading of the accounts reveals a reported turnover of €53,670m [4]. Of that, Thomas Pink represents a quarter of a percent. While Covid has killed demand for shirts, the MH in LVMH's name stands for Moet and Hennessy, and the various brands of alcohol that the group sells may have done very well while people have time on their hands at home. [5]

So why does it matter if this tiny subsidiary expired? LVMH's consolidated accounts show that in aggregate the group is respectably profitable, and it has ample resources to weather a loss in an obscure corner of the empire. It earned more per week in 2019 than Thomas Pink lost in the whole of its existence.

We don't think it's that simple. That a business consolidates a smaller one into its own accounts does not grant it unfettered access to the smaller one’s assets. Its directors have to run that company as they would if it was independent of the parent. In particular, they have to give thought to their company's creditors. While two businesses may have shared ownership and identical directors, they are most unlikely to have the same customers, employees, landlords and other suppliers.

That's not to say that a company can't draw on the resources of a group that it forms part of. A parent may provide letters of support, and guarantees, and money can be loaned in and out and moved between subsidiaries that make money and those that need it. But all of these arrangements need to be defined contractually, and to make sense from the narrow perspective of each of the companies involved in them. A business will not have achieved the scale and success of LVMH without having these arrangements well ordered and carefully documented.

From the point of view of the top company in a conglomerate, everything is a subsidiary, and the only income it has is a blend of dividends and fee income of the kind we are here contemplating. It is on this pinnacle, balanced perhaps delicately on the rest of the edifice, that shareholders are relying to receive their flow of dividends.

Several large property companies specialising in retail malls have expired recently. In almost all cases, they were in mortal peril as a result of changing shopping habits, but the immediate cause of failure was the combined effect of internal inter-company arrangements which had made sense during the good times but choked them when things turned sour. It is not enough for a group of companies to report adequate profits on a consolidated basis. It only needs one obscure unit to breach its loan covenants for the whole thing to be seized by a coronary attack of lock-ups, cross-guarantees and defaults. The risk is that these contracts rest on assumptions about what was the status quo, which have become invalidated by Covid. Now, they form a cholesterol-like blockage to the flow of funds within the organisation.

Companies can't simply rewrite these agreements, for example to move more money from flourishing subsidiaries to ailing ones, or to increase the management charges that they levy on subsidiaries, because the directors of the entities providing the funds have to justify why the change makes sense to their businesses in isolation.

So we are left wondering how many of the subsidiaries of complex international businesses are being dragged under water by management fees, fees that the corporate centre depends on to recover the costs it needs to meet, to run itself and to provide the group-wide brand management that is the whole point of businesses of this kind.

These issues will be more topical in companies the more complex, carefully calibrated and international are their structures. Pressures will apply particularly as businesses seek to rebuild their activity levels when the pandemic abates, since most firms that are growing, or re-growing after this year of shrinkage, consume cash as they replenish their depleted working capital pipelines.

Relaunch

As we have seen, succeeding years' annual reports described repeated attempts to relaunch Thomas Pink and reverse its losses. One thrust has been to take the business upmarket. In the end, from a start offering lower prices as a result of avoiding a costly Jermyn Street presence, Pink came to have what looked like the largest store on Jermyn Street, and prices higher than many of its neighbours. In this way the value proposition which led the firm to its original success was completely inverted.

It is this that the holding page for the Thomas Pink website is no doubt alluding to when it leads with "Don’t fret—we’ll be back soon. We're excited to announce that we’re returning to our roots ..."

Lessons

We draw six lessons from this saga.

Thomas Pink had been racking up losses for years before any pandemic relieved work-from-home customers of a need for new shirts.

How those losses could have amounted to £100m from a couple of dozen shirt shops collectively turning over no more than £10-20m is itself an interesting question.

Covid provides a convenient excuse for closing businesses that were marginal already. Or, Covid can be said to accelerate changes that were on the way anyway.

It is possible for conglomerates to report good looking consolidated financial statements but still suffer life-threatening cash flow constrictions internally.

Questions of governance and going concern apply as much to individual units as they do to the top holding company, and can be challenging to address at the moment.

The distinct competence claimed by large fashion brands, to be able to acquire businesses that are appreciated locally and make them sought after on a global scale, doesn't work in every case.

What next?

A distinctive feature of Pier Review is that it provides the financial model that underpins each analysis.

Because Thomas Pink is not quoted, the spreadsheet for this article is small, and concerns itself with deriving the direct cash flow from the income statement, balance sheet, and notes to the accounts.

To receive the spreadsheet

if you have not done so already, subscribe to Pier Review by using the box below

click here to pre-populate a message in your usual email program requesting that the spreadsheet be sent to you

switch to your email program and click Send to despatch the request.

If you find this analysis interesting, you can sign up to have others like it delivered to your inbox several times a month.

Share Pier Review with interested friends.

Notes

[1] Thomas Pink divides its costs between cost of sales, distribution and administrative costs. To get these figures from the accruals basis on which they are presented to an indication of cash flow, it is necessary to adjust them. Publicly available information is enough to work out these adjustments in aggregate, but allocating them between the three cost categories requires some educated guesswork. We have assumed all property costs relate to shops and warehousing, and so are a form of distribution cost. We are implicitly assuming that the cost of Thomas Pink’s head office, which is likely captured within administration costs, forms a negligible portion of total property costs.

[2] At one time Thomas Pink had many more stores as a result of franchising arrangements but it withdrew from them.

[3] Thomas Pink has withdrawn from train stations as part of its move up market, but that’s where it was for much of the period addressed in this article.

[4] This is for 2019. LVMH has already published its 2020 accounts, but Thomas Pink has not and we wanted to use a consistent period for comparison.

[5] Counterargument: the LV stands for Louis Vuitton; which has probably been selling little luggage in recent months.

I spoke to a salesperson in Nov18, when the company "elevated the brand" by doubling prices overnight. Absolutely nothing else changed, but a white shirt went from £80 to £160. Same fabric, same manufacturing, just targeting a different customer. The product had already been "value engineered" in preceding years, so was no better than the £25 equivalent from TM Lewin et al.