Shell

Revenues halved and a large loss; but cash metrics are undented

As regular readers know, the enthusiasm of Pier Analysis for the wonders of the leading technology companies does not extend to their share prices. Might better value be found among companies that are less fashionable?

Circumstances don’t come much less fashionable than this:

Shell’s profits were $24b in 2018 and $16b in 2019, but in 2020 they fell sharply into loss of $22b.

The company’s share price, having peaked at over £27 in May 2018, reached a low of £10.62 in March 2020 as Covid played havoc with demand for, and the price of, oil and related products.

If you had put $100 into Shell when it was at that May high, you would now have $47. The same investment in Apple on the same date would be worth $263. Today, your Apple holding would now be worth 5.5 times as much as your Shell holding.1

Some argue that the FATMAAN stocks are the future; the oil majors are the past, and will find their assets stranded. Political pressures and climate change concerns will make expensively discovered reserves of oil and gas unextractable. Excellent. We like unpopular shares.

Enterprise value

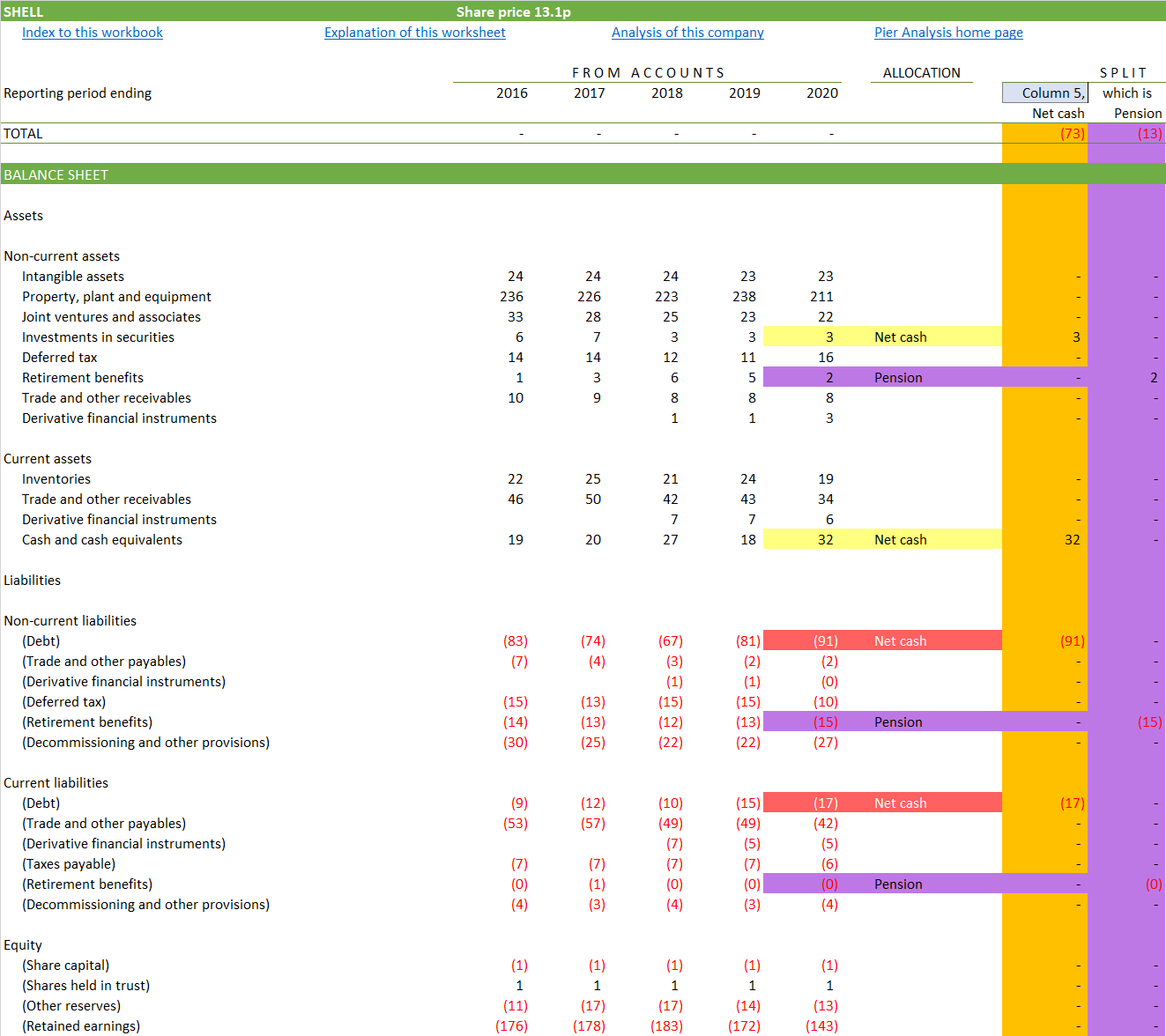

Our investigation of whether Shell has any promise starts with its balance sheet.

Highlighted in red: Shell has $108b of debt.

Highlighted in yellow: Offsetting this, Shell has $35b of cash and investments.

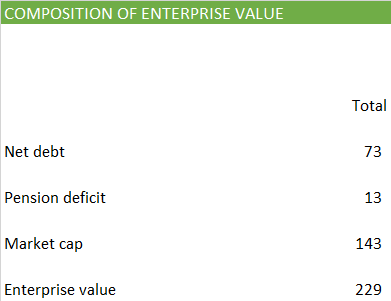

Highlighted in orange: Together, these things give a net debt position of $73b.

Highlighted in purple: It also has a net pension deficit to the tune of $13b. Pier Analysis regards obligations to former employees as just as much a debt of the company as money owed to its conventional lenders.

To these we add a third constituency, the shareholders. The amount they have at stake in the business is measured by Shell’s market capitalisation. Shell has two classes of share.

A shares are denominated in euros and quoted on Euronext in Amsterdam.

B shares are denominated in sterling and quoted on the London Stock Exchange.

These euro and sterling amounts need to be converted into dollars, as we want to compare them with Shell’s accounts. Because the oil price is quoted in dollars, pretty much all companies in the oil business present their numbers in that currency.

Whenever there is more than one class of share, or there are currency conversions involved, as are both the case for Shell, Pier Analysis works out the company’s market capitalisation from first principles. The usual providers of data are inclined to make a mess of it, or to be unclear about which currency they are using to present the values or which class of share they are talking about.

Highlighted in yellow: The current share prices are €16.81 for the A shares and £13.44 for the B shares.

Highlighted in green: We find that Shell’s overall market capitalisation is $143b.

Highlighted in red: By way of illustration of the haphazard estimates of the different data providers, Google thinks the B shares are worth nothing and the A shares are worth 128b, which is a reasonable estimate of the two classes combined in Euro terms.

When we combine these three figures, we find an enterprise value of $229b.

Required cash flow

Banks and other lenders such as bond holders should lend money to Shell only if they judge it capable of generating cash flow sufficient to provide

progressively, over time, repayment of the debt

during the time that that takes, payment of interest at a rate that offsets what it costs them to raise the money and covers the loans that go wrong.

Much the same is true for investors. They should place their money with Shell only if they expect that it can

eventually, over time, return it 2

provide an additional return on the investment sufficient to compensate them for the risks they expose themselves to, and the other opportunities they forego, by tying their money up in the company.

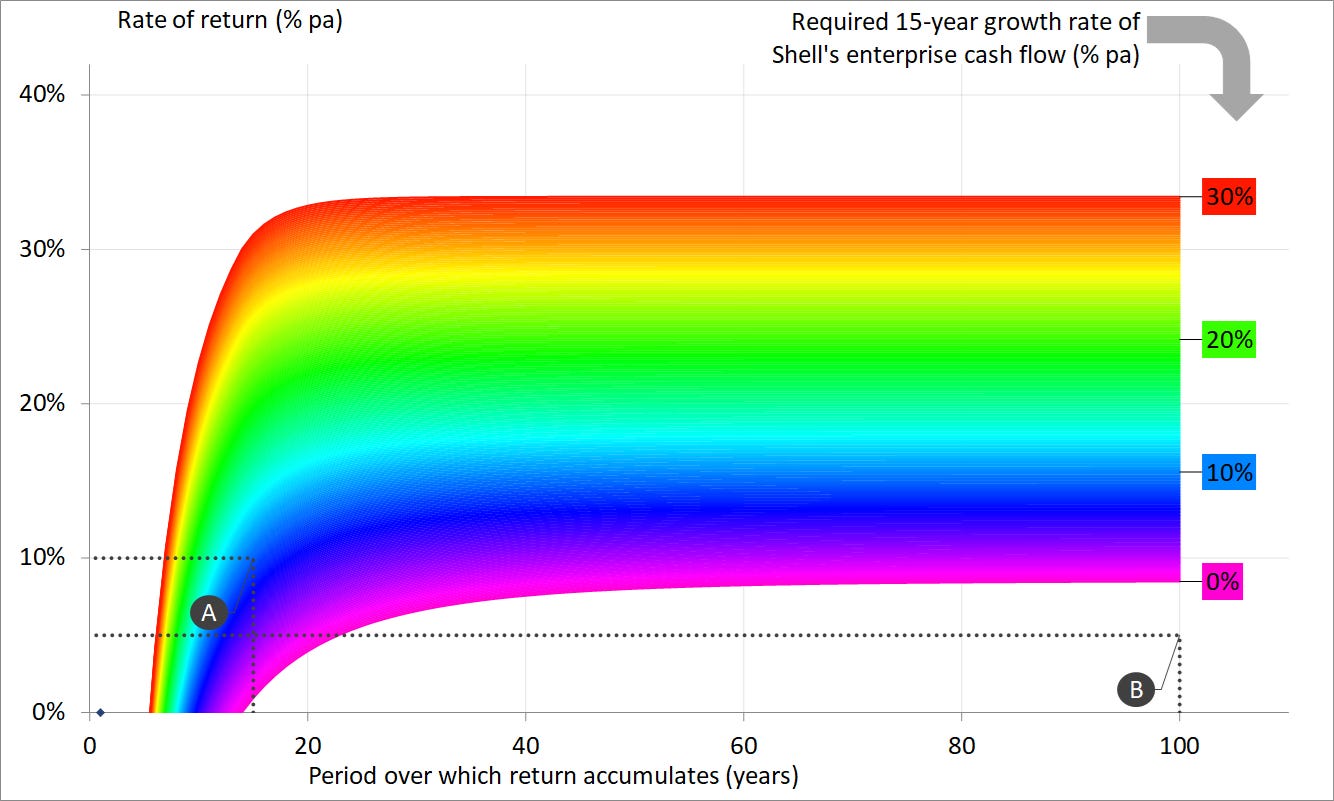

How long should investors be willing to wait for this return of their investment? Pier Analysis wants it completed within 15 years 3, and it seeks a rate of return on top of that of 10% pa 4.

These requirements are much more conservative than are typical, and that is particularly so in current exuberant markets. That is by design, in pursuit of a large margin of safety. An exhibit at the end of this article will show what Shell looks like to the majority who are content to accept less demanding requirements.

Given all of this, for Pier Analysis to consider that the current $229b enterprise value is justified, it would need to find plausible the idea that Shell can deliver cash flows, over the next fifteen years, which have a net present value of that same $229b when discounted at 10%. One way Shell could manage this is to deliver cash flow of around $28b to $33b. This is the violet line on the chart below.

Another way to accomplish it is to provide a cash flow that starts much lower, at around $12b, but compensates for that fact by finishing much higher, at around $41b as a result of growing very much faster. This is the red line on the chart. We concentrate the growth in the next five years.

The other colours show hundreds of equally valid permutations between these extremes. There exist infinitely many more beyond those that are not drawn on the chart.

Actual cash flow

Now that we know roughly what cash flow Shell needs to deliver to justify its current valuation, we can take a look to see what it has actually managed in recent years. As we have seen, Shell has reported significant losses, but Pier Analysis has almost no interest in measures of profit. It focuses on cash flow.

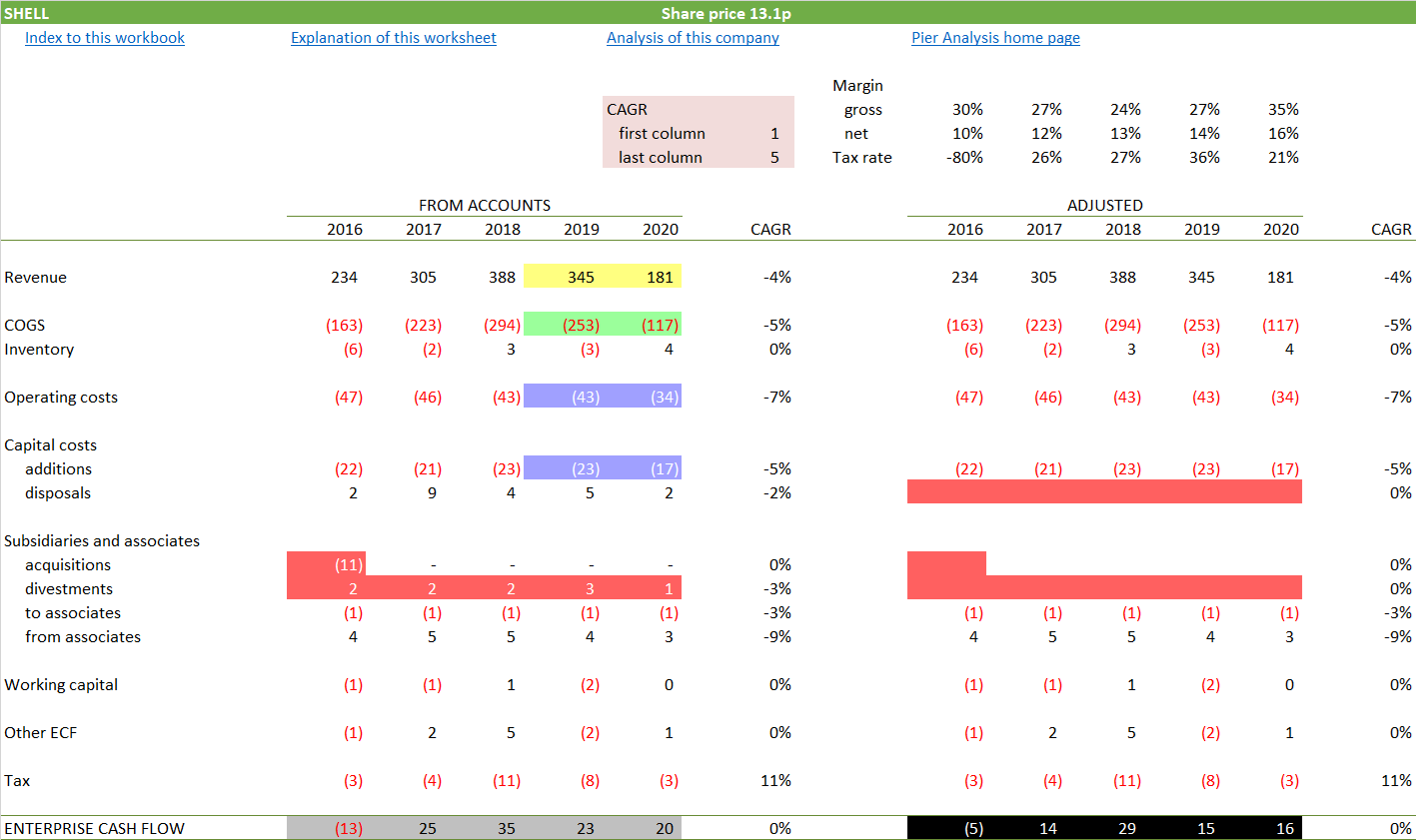

On the left below is what the accounts show, after we have restated the cash flows from the accounting profession’s impenetrable indirect format into an easy to understand direct layout.

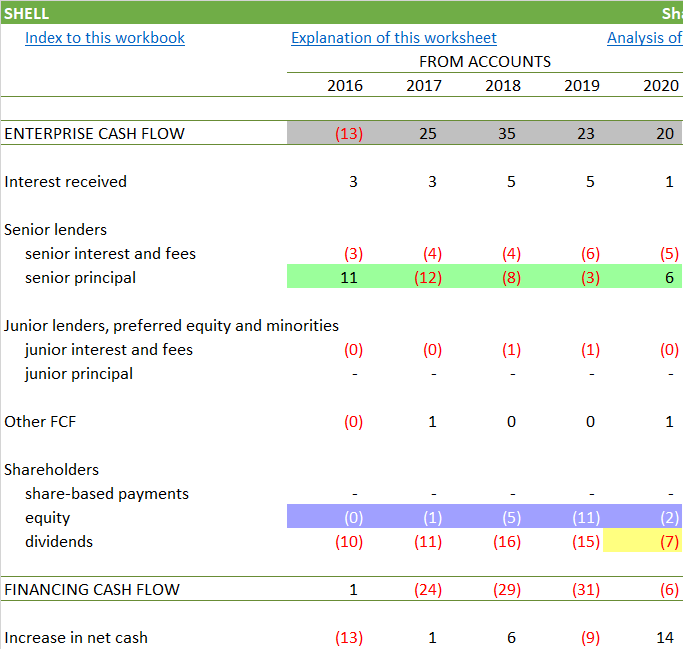

Highlighted in yellow: Having grown at 15% pa between 2016 and 2019, Shell’s revenue nearly halved in 2020.

Highlighted in green: Since volumes fell, the cost of supplying them inevitably declined too.

Highlighted in blue: Shell took a firm grip of its operating costs, reducing them by 19%, and its capital costs, reducing them by 28%.

Highlighted in grey: As a result, Shell delivered enterprise cash flow of $20b, which was only 11% down from the previous year. We consider this a remarkable result.

Highlighted in red: In the search for a measure of Shell’s underlying cash generation capability, we show on the right a version of the cash flow which is adjusted to eliminate items that cannot be relied on to recur. In this case our adjustments are confined to removal of the cash flows resulting from

the acquisition of British Gas in 2016

the proceeds of asset disposals

the proceeds of divesting unwanted businesses.

Highlighted in black: The adjusted version of the enterprise cash flow is $16b, which is, astonishingly, higher than the previous year, and better than the average of the previous four years. This represents a cash yield on enterprise value of 7.7%.

Plausibility

We can now represent these grey- and black-highlighted cash flows as grey and black lines alongside the rainbow-coloured required future cash flows already shown.

The rightmost section of the black line, circled, reflects the slightly improved adjusted cash flow just mentioned. Looking at this graph shows that the story isn’t about how Shell did in Covid 2020 compared with pre-Covid 2019. The question is what represents a long-run cash flow for the business. Is it the $30b peak that was seen in 2018? Or is there a chance that the negative times of 2016 could return?

If one believes that the $30b is representative, and Shell’s cash flow will bounce back to that level the moment Covid is conquered and stay there, then the company is a howling buy. The comparison of interest on the graph is between the peak of the black line at $30b, and the violet lines, which start at around $28b and grow gently to $33b. In this scenario, the company is already delivering more than it needs to justify its current valuation, or rather will do so as soon as the world is released from confinement.

If alternatively one takes the view that the Covid-depressed $16b is the new base line, the lines of interest are the green ones. They show how the cash flow needs to grow from its current levels to justify the valuation. It needs to head up well beyond where it was in 2018, to just beyond $40b.

Pessimists will take the view that the area of interest in the graph is the left edge, where 2016 shows that Shell is perfectly capable of generating negative cash flows, and those days will return as political pressures mount on the environmental front. Cars, these people say, will become electric; many countries have announced an intention that internal combustion engines will cease to be sold from various dates between 2025 and 2050.

The world will have no need of the toxic products of the oil majors. Pier Analysis claims its insistence that companies can justify their valuations with fifteen years’ worth of cash flow is conservative, but, the pessimists (or, as they will see it, optimists) say that even this is longer than oil and gas extraction will be tolerated.

Choosing

In choosing between these alternative possible futures, Shell’s annual report is our friend.

First, we need to understand what has driven the swings in revenue. The issue is only secondarily demand for oil and gas. Shell’s production dropped 7.4% in 2020 but its revenues halved. The reason is that the oil price plummeted because of an increase in supply and the Covid decline in demand. At some points in the year the oil price became briefly negative.

Shell’s description of this context is nicely written and interesting. Since it is rather long to be quoted in full, it is put in Appendix A to this newsletter.

Clearly if oil remains in oversupply, producers will have to remove capacity, starting with the most expensive. But that is a secondary effect. In the medium term at least, the bet is much more about oil prices than it is about production volumes.

In the longer run, the turn away from oil will no doubt gather pace. Shell’s annual report devotes 14 pages to climate change and energy transition. Only the report on remuneration and the financial statements themselves are longer. Highlights are reproduced in Appendix B. It’s a larger extract than we would commonly reproduce, but central to forming a view as to whether Shell will be defeated by climate change concerns or play a leading, essential and profitable role in addressing them. In our view, its case that it can be the solution rather than the problem is persuasive.

We started this article comparing Shell with fashionable and highly priced tech stocks. Within not particularly onerous limits, Apple can charge what it likes for its products and services. Oil companies, by contrast, have almost no pricing power. They are subject to geopolitical forces and a market in oversupply from which governments have little incentive to encourage their own national protagonists to withdraw.

Financing

We should look to see what Shell has done with the enterprise cash flow it generated.

Highlighted in grey: The enterprise cash flow at the top of this part of the cash flow picks up from the figures, also highlighted in grey, at the bottom of the previous cash flow.

Highlighted in green: Shell has been steadily retiring debt, except last year when it drew down more new debt than it repaid. However, the bottom line of the cash flow shows that the debt so drawn is more than offset by increased holdings of cash. In other words, Shell has drawn down these borrowings but not yet spent them. Net, Shell managed to reduce its debt in 2020, despite halved revenues.

Highlighted in yellow: To use its own language, Shell “rebased” its dividends last year. It has laid out clear criteria for resuming growth in this dividend, once it has paid down more debt, maintaining it at roughly today’s fraction of cash flow.

Highlighted in blue: Shell had been buying back shares, something that has stopped as it puts a tight control on cash. This is arguably back to front. Shares are better bought now, when there is a case to be made that they are undervalued, than a year or two ago, when they were more than twice the price.

At today’s valuation the dividend yield is 5.2%. This can be interpreted in several ways.

One is that investors have reacted to the shocking results, in terms of a collapse in turnover and profit, without perhaps understanding how undamaged the cash flows have been.

Another is that the market does understand the cash flows, but doesn’t believe that they can be sustained, or will be permitted to continue for much longer. Shell can try its transition, but won’t make it, or will make it but will find itself thereby in new activities which, with lower barriers to entry (almost nothing is as hard as erecting deep-sea oil platforms), will enjoy much smaller margins. One possible counterargument is that engineering hydrogen distribution networks with national or continental coverage is pretty hard; the acquisition of British Gas gives it expertise in transmission networks of this kind, and ownership of places where drivers can fill up with petrol is handy if some of them will one day fill up with hydrogen.

A further possibility is that oil companies are becoming pariah stocks, uninvestible by funds with large ESG sensitivities just as coal mines are already. For those with the mindset that their holding period is forever, what happens to the price once they have bought the share is of little concern. Their interest is in acquiring a stream of future cash flow, and paying little for it would be welcome. In this context Merryn Somerset Webb’s article Want a greener world? Don’t dump oil stocks (FT, needs subscription) is very recommendable.

Conclusion

As already acknowledged, the criteria that Pier Analysis applies are unusually demanding. They are represented by point A in the chart below: a requirement that the company generates cash flow sufficient to provide a 10% pa return on enterprise value over fifteen years. The point lies on the blue contour, which, the annotations at the right show, correspond to a requirement that Shell’s cash flow can grow from current levels at around 8% pa.

Point B shows what the position looks like to those who are willing to tie their money up in the company indefinitely, and would be content with a return of just 5% pa on the grounds that it is at least more than they are getting from bank deposits. Because Shell’s cash yield on enterprise cash flow is already over 7%, the cash flow would have to contract significantly if it were to deliver a return of only 5% pa over an extended period. From the point of view of these investors, Shell is priced to shrink.

Shell will indeed shrink if the oil price languishes for want of demand for the stuff or if the oil majors are effectively driven out of business by climate concerns. Might those things happen? Of course they might. We though are much more inclined to believe in an oil price sustained by a resurgent economy (even before recovery, it’s already back above the average for 2016-2019), and in Shell being among the winners in repositioning itself to be part of the solution in the climate change agenda. If it can manage to keep its cash flow unimpaired in a year when Covid halved its revenues and turned oil prices intermittently negative, it would seem to have the management discipline to make the renewables transition.

Thanks to Roger Mayhew for suggestions and pointers as the draft of this article evolved.

What next?

Comments are always welcome, both on the reasoning behind this article, and, this week, a particular question: we are contemplating trialling Clubhouse as a forum for discussion of this and similar articles and would value an indication of whether that would attract any interest.

A distinctive feature of Pier Review is that it provides the financial model that underpins each analysis. To receive the spreadsheet

if you have not done so already, subscribe to Pier Review by using the box below

click here to pre-populate a message in your usual email program requesting that the spreadsheet be sent to you

switch to your email program and click Send to despatch the request.

If you find this analysis interesting, you can sign up to have others like it delivered to your inbox several times a month.

Share Pier Review with interested friends.

Appendix A: Crude Oil

Taken from Shell’s 2020 annual report, slightly reformatted for readability

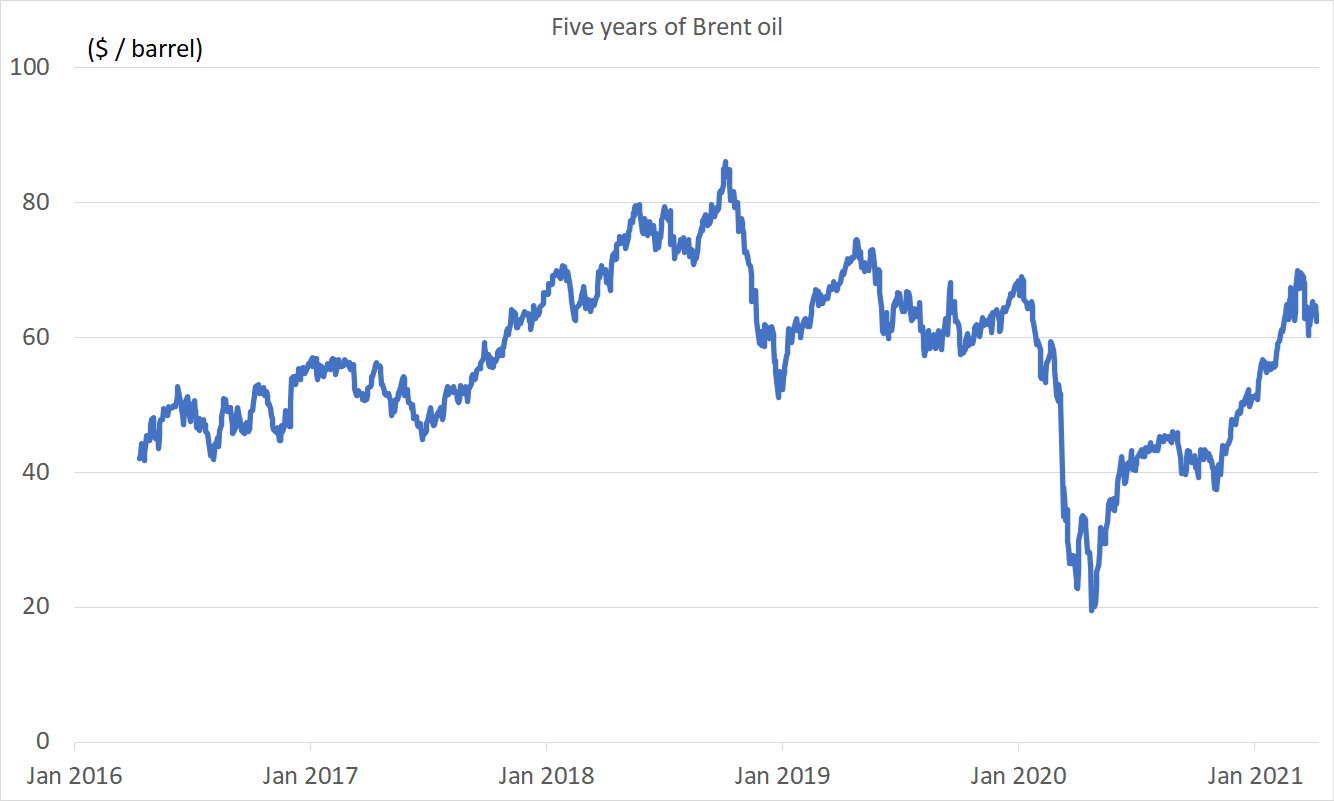

On a daily average basis, Brent crude oil, an international benchmark, traded between $13 per barrel (/b) and $70/b in 2020, ending the year around $50/b. Brent crude oil prices averaged $42/b for the year, 34% (or $22/b) lower than in 2019.

In 2020, oil markets experienced unprecedented developments in demand driven by the COVID-19 pandemic.

At the start of 2020, global oil demand for the year was expected to grow by 1.2 million barrels per day (b/d). Then in January, oil demand started to contract because demand fell in China as lockdown was imposed to contain the virus outbreak.

In subsequent months, oil demand contracted further as the outbreak in China evolved into a global pandemic and lockdowns were introduced across the world.

In April, oil demand fell to its lowest level, around 22 million b/d below year-average demand in 2019, according to an estimate of the International Energy Agency (IEA). Contraction of such magnitude has never been recorded before.

Country lockdowns deeply impacted transportation sectors, especially passenger road and passenger air in Organisation for Economic Co-operation and Development (OECD) economies.

In subsequent months, oil demand started recovering, but only partially, because resurgences of COVID-19 triggered re-imposition of social distancing and travel restrictions.

By the fourth quarter, global oil demand was still estimated to be around 5.5 million b/d below the 2019 level, according to the Oil Market Report published by the IEA in January 2021. Averaged for the full year, oil demand contracted by around 9 million b/d, or 9%, to 91.2 million b/d. Oil demand fell by 5.7 million b/d in OECD economies, and by 3.2 million b/d in non-OECD economies. By contrast, oil demand in 2019 was 0.8 million b/d higher than in 2018.

In 2020, oil markets also experienced unprecedented developments in supply.

In March, there was a serious disagreement within the OPEC+ alliance, which consists of OPEC members and co-operating non-OPEC resource holders such as Russia. Saudi Arabia and Russia failed to agree on what to do about falling demand for oil. Saudi Arabia responded to the disagreement by boosting its production to almost 12 million b/d, a monthly record. By April, storage capacity was filling up quickly and oil prices were falling rapidly.

On April 12, the OPEC+ alliance agreed to jointly reduce production by an unprecedented 9.7 million b/d for May and June.

For the month of June, Saudi Arabia voluntarily cut production further, by around 1 million b/d. For the rest of the year, the OPEC+ alliance agreed on and complied with a production cut of 7.7 million b/d. notably in the USA. The US Energy Information Administration reported a supply contraction of around 2 million b/d by the end of May, from a level of around 13 million b/d at the start of the year.

US producers cut budgets, leading to an unprecedented fall in the number of oil drill rigs to around 26% of the total at the start of the year. Supply from the USA occasionally fell even further to around 10 million b/d because of production shut-ins during the hurricane season.

In aggregate, production of oil supply in 2020 is estimated in the Oil Market Report at 93.9 million b/d, which is 6.7 million b/d lower than in 2019. OPEC production is estimated to have fallen by 3.8 million b/d. Supply from the USA fell by 0.8 million b/d from 2019. By contrast, global oil supply in 2019 was 0.1 million b/d higher than in 2018. Daily average oil prices reached a low at the end of April before the OPEC+ supply curtailments came into effect. Brent crude oil prices fell to around $14/b. Contract prices of some crude grades, such as West Texas Intermediate (WTI), even traded well below $0/b for a short period.

Brent crude oil prices started to recover from May and traded in a price range of around $35-45/b from June. Towards the end of 2020, announcements of promising COVID-19 vaccines supported Brent crude oil prices, allowing them to break through the upper end of this range.

On a yearly average basis, WTI crude oil traded at a discount of about $2.5/b to Brent crude oil in 2020, compared with $7/b in 2019. The discount narrowed from 2019 because falling US supply prevented bottlenecks in pipeline capacity from the landlocked Cushing storage hub to the US Gulf Coast. According to the US Energy Information Administration, US crude oil exports increased further to a yearly average of around 3.1 million b/d in 2020, up by 0.1 million b/d from 2019. This helped to ensure a narrow price differential between Brent and WTI.

Looking ahead, the IMF’s global economic outlook indicates some increase in global economic growth, which should support oil demand growth.

Demand growth could accelerate further if vaccines can help contain COVID-19 and allow a return to pre-pandemic demand patterns in perhaps two or three years. According to the IEA, global oil demand is projected to increase by around 5.4 million b/d for 2021 to reach 96.6 million b/d. This is still 3.4 million b/d less than in 2019. OPEC+ members may have to carefully balance supply growth with sustained production curtailments in order to achieve price stability.

In the near term once demand has recovered to 2019 levels, the need for OPEC+ cuts may diminish. If there is further demand growth, tightness of supply could even develop. This is because any supply growth from the US shale basins could be limited, since US operators have shifted their focus from volume to value. We expect this shift to be permanent.

The supply growth potential from outside OPEC+ and the USA could be limited by industry-wide lack of investment in new supply projects which also tend to have a long lead time.

In the near term, prices could rise if demand is quicker to recover and OPEC+ members successfully constrain supply. On the other hand, the price environment could weaken if the impact of COVID-19 prevents full demand recovery, and/or OPEC and the non-OPEC resource holders relax their production agreement. The price environment could also weaken if there is an increase in supply from other non-OPEC producers, such as US shale producers.

Appendix B: Shift to renewable energy

Taken from Shell’s 2020 annual report, slightly reformatted for readability

Shell has long recognised that greenhouse gas (GHG) emissions from the use of hydrocarbon-based energy are contributing to the warming of the climate system. … We welcomed the efforts made to reach … and fully support the Paris Agreement’s goal, to keep the rise in global average temperature this century to well below 2 °C above pre-industrial levels and to pursue efforts to limit the temperature increase even further to 1.5 °C.

In pursuit of this goal, we also support the vision of a transition towards a net-zero emissions energy system. Shell agrees with the statement of the Intergovernmental Panel on Climate Change (IPCC) special report, Global Warming of 1.5°C, that says that in order to limit global warming to 1.5°C above preindustrial levels, the world economy would need to transform in complex and interconnected ways. Meeting this challenge would require an even more rapid escalation in the scale and pace of change in the coming decades than was foreseen in the Paris Agreement.

Shell recognises that society’s attitude towards climate change is shifting rapidly and that it is different in different locations. Regulators in some advanced economies such as the EU and the UK have already started pushing for net-zero emissions by 2050 in an effort to achieve the 1.5 °C stretched goal of the Paris Agreement. Potential similar developments in other key locations might lead to similar or more stringent regulatory conditions on Shell’s operations and products.

On February 11, 2021, we announced … our new strategy … to accelerate progress to net-zero emissions, purposefully and profitably. One of the pillars of this strategy is for Shell to become a net-zero emissions energy business by 2050, in step with society. … This will require us to transform our business, working with our customers and others, in sectors that are difficult to decarbonise. This includes aviation, shipping, road freight and heavy industries.

We also believe that our total oil production peaked in 2019 and our total emissions (Scope 1, 2 and 3) peaked in 2018 at around 1.73 gigatonnes per annum. Shell’s target is to be a net-zero emissions energy business by 2050, in step with society. This means net-zero emissions from our operations – our Scope 1 and 2 emissions – and also net zero from the end use of our products that we sell – our Scope 3 emissions. Our Scope 3 emissions include our customers’ emissions from the energy products we produce and sell as well as the life-cycle emissions of the energy products produced by other companies that we resell to our customers. This means that our target covers all the energy we sell, not just the oil and gas we produce and refine ourselves.

But Shell cannot get to net zero without society also being net zero. While we aim to transition slightly ahead of society, where we expect to see higher margins for our low-carbon and renewable energy products, we cannot transition too quickly or we will be trying to sell products that our customers do not want. Accordingly, other than our short-term remuneration targets, all targets are conditional on being in step with society. If society is not on the path to net zero for 2050, it is unlikely that Shell will meet its emissions targets.

We believe it is important for the Board and the management to understand what our shareholders think. Accordingly, in 2021, Shell intends to submit its energy transition strategy to shareholders for an advisory vote at our Annual General Meeting. We will submit our energy transition strategy to such an advisory vote every three years. We will also seek an advisory vote on the progress we make each year, as disclosed in our Annual Report, starting in 2022.

Our target is to be a net-zero emissions energy business by 2050, in step with society. We aim to achieve these targets in step with society. They are:

net-zero Scope 1 and Scope 2 emissions from our operations by 2050; and

net-zero Scope 3 emissions from the energy products we sell by 2050.

We are taking steps to cut emissions from our existing oil and gas operations, and to avoid generating more in the future.

We believe our annual oil production peaked in 2019, and we expect our total oil production to decline by 1-2% a year until 2030.

We do not anticipate any new frontier exploration entries after 2025.

Natural gas is the least polluting hydrocarbon. We expect the percentage of total gas production in our portfolio to gradually rise to 55% or more by 2030.

By 2030, we will end routine flaring of gas, which generates carbon emissions, from the assets we operate.

By 2025, we expect to have kept the methane emissions intensity of Shell-operated assets to below 0.2%.

Getting the energy system on a path to net zero will require co-ordinated action between energy providers, energy users and governments. They will need to work together over the coming decades to define rapid, realistic decarbonisation pathways, sector by sector.

We will work with our customers to address the emissions created when they use products bought from us (Scope 3) and help them find ways to reduce their emissions and overall carbon footprint to net zero by 2050.

We are already taking steps to cut emissions from our existing oil and gas operations, and to avoid generating more in the future. We aim to reduce the GHG intensity of our portfolio and we continue to work on improving the energy efficiency of our existing operations. One element of our target is to achieve net-zero emissions from all our operations, as well as from the energy we need to power them.

Shell believes that society must accelerate and increase the scale of all forms of GHG reduction. We are increasing the proportion of lower carbon products such as natural gas, biofuels, electricity and hydrogen in the mix of products we sell.

Our shift to energy and chemicals parks means we will reduce our production of traditional fuels by 55% by 2030, from around 100 mtpa to 45 mtpa. We plan to build on Shell’s leading position in hydrogen by developing integrated hydrogen hubs to serve industry and heavy-duty transport, aiming to achieve double-digit share of global clean hydrogen sales.

Our marketing platform is one of the best in the energy industry. Spanning 160 markets, every day we serve more than 30 million customers at our retail sites; and one million businesses. Our customer access gives us first-hand insights, helping us to deliver what our customers want rather than offering what others think they need. This will help us to grow our existing marketing platforms profitably, while also increasing the decarbonisation choices across sectors and countries.

Our global ambition is that by 2025 we are operating more than half a million electric-vehicle charging points for businesses, fleets and customers, at our retail sites and people’s homes. This number is expected to rise to 2.5 million charging points operated by Shell by 2030.

Our approach to commercial road transport is similar to how we work with other hard-to-decarbonise sectors such as shipping and aviation. We are working with transport companies, truck manufacturers and policymakers to identify profitable pathways to decarbonisation.

We are already one of the world’s largest blenders and distributors of biofuels, and we will continue to invest in and increase the production of these low-carbon fuels. Over the next decade, we will help customers in Europe, China and on the US West Coast to transition to liquefied natural gas (LNG) and biogas.

Hydrogen also offers a route to lowering emissions. We are part of the H2Accelerate consortium, which looks at ways to create infrastructure for generating and supplying hydrogen across Europe.

We are also supporting infrastructure development through our investments in Silicon Ranch and Cleantech Solar. Combined, these two companies have over 350 solar farms in the USA and South-east Asia. In Australia and in Oman, Shell is building its first large-scale solar farms.

Shell’s infrastructure, systems integration, experience and people put us in a strong position to profitably meet the current and future needs of our customers, helping them and society to decarbonise for a net-zero emissions future.

Not quite. We’ve looked at the way the share prices have moved in whatever currency they are quoted and ignored exchange rate movements.

Even those who intend to sell the shares rely on the existence of others who believe that the company is good for repayment of whatever they put into it.

Standard practice in the investing community is equivalent to being willing to wait for ever. Pier Analysis takes the crabbier view that companies are not immortal, and wants its money back over fifteen years. This is in effect what is on offer from funds specialising in power, transportation and social infrastructure such as schools and hospitals. They invest in projects which typically have lives of around thirty years, and the average project will be half way through that life. Pier Analysis considers these funds to be appropriate alternatives against which other investments can be calibrated.

This is much higher than most investors seek in current markets. Pier Analysis chooses this rate because it is the kind of figure available from the infrastructure funds that it considers to be appropriate alternatives against which other investments can be calibrated.