This note is part of the Pier Review reference material.

It is aimed at beginners. If you are familiar with the terms TVM, DCF and NPV, you already know this topic.

An infinite amount of money

Ben is an editor at a small newspaper. Under pressure from digital media, sales are falling. He hopes to reverse this trend, or at least slow it down, by running some kind of competition. Every week, he intends to offer $20,000 to the winner of a difficult quiz or crossword. That means his business is going to give away about $1m every year.

Ben realises that once he has started, it is going to be difficult to retract this prize, so if he begins the competition, he is committing his paper to it for many years. How much money does he need to put aside in order to be sure he can meet this obligation? One answer is that if he is going to offer the prize for an unlimited number of years, we need an unlimited amount of money.

There is no way Ben is going to persuade his colleagues, and the owners and directors of the newspaper, to commit to giving away an infinite quantity of cash. This seems an insurmountable obstacle in the path of the idea.

Bank to the rescue

Contemplating this problem morosely as he headed home, Ben passed a bank. In its window he noticed a sign that promises 2% interest on any deposits. It dawned on him that if he put $50m into that bank, 2% would generate $1m of interest within a year. He could give that to the newspaper’s prize winners, and still have $50m in the bank, which will generate a further $1m, not just next year and the one after, but in every year, for ever.

How do we reconcile the fact that Ben thought he needed an infinite of money to offer prizes indefinitely, and now sees that he can do the same job with $50m?

Ben’s error was in the first argument. He added together $1m this year, and $1m next year, and $1m thereafter, and so on forever. But $1m this year should not simply be added to $1m next year, because in a sense they are not comparable. Given the choice between $1m that arrives right now and $1m that doesn’t arrive until a year has elapsed, rational people would prefer the $1m now. Among reasons for the preference are that

as we have just seen, they can put the money in the bank and be earning interest on it

they could spend it on something they fancy, rather than having to wait

they might not be alive in a year’s time to receive the money

the bank might not be alive in a year’s time to give them the money

A dollar today is worth more than a dollar tomorrow

Economists recognise that money is worth more if it arrives (or leaves) immediately, and worth less if it is arrives (or leaves) at some time in the future, by discounting it. $1m, in cash, right now, is worth, unambiguously, $1m. But £$m that won’t arrive for a year is worth about $980,000. [1] This is the result of taking the $1m and dividing it by 1.02, chosen because we have already mentioned that the interest rate is 2%.

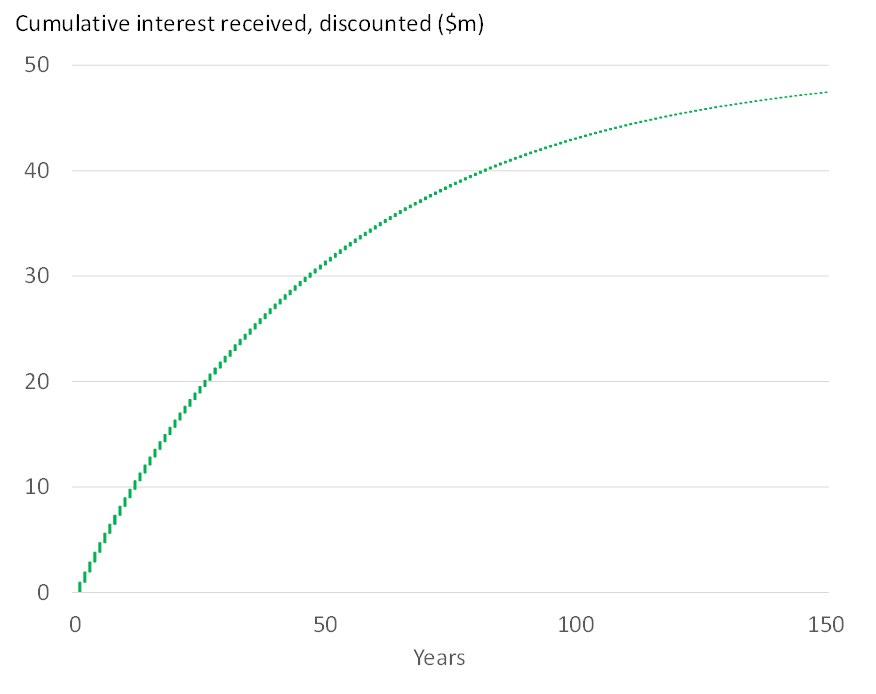

$1m that arrives in 2 years time is worth about $960,000 [1], being the $1m divided by 1.02 representing the coming year and another 1.02 representing the year after that. Each year, we divide the $1m by a discount factor, which starts at 1.02, then 1.0404, and gets bigger ever year. The series of $1m that we need to pay out to prize winners every year are called future values. When we discount each of them back to today’s value, we get a collection of what are called present values. If we take a series of present values, as we have here, and add them up, we get what is called a net present value, or NPV.

Let’s have a look at the build up of net present value as we add years to this analysis. After $1m, we have $998,000. [1] After two years we have $1,994,000. As we keep going, we see over many years we wind up with a graph that curves towards $50m for discounted pounds. We can go on adding present value indefinitely, but we’ll get ever closer to the $50m, but never go past it, because the discounting is making the present values tinier and tinier.

That $50m is the number that we agreed would generate $1m pa if we put it in a bank account that yielded 2% pa. That’s not an accident; it’s how the maths works. The way interest compounds, and discounting, are mirror images of each other.

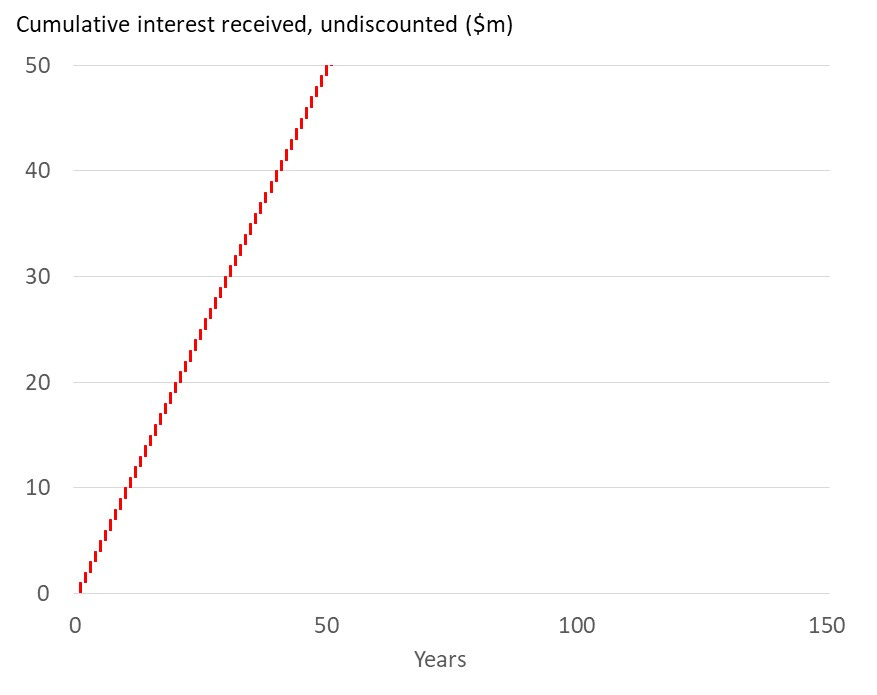

If we don’t discount the cash flows, the annual amounts are all the same size. The accumulation climbs linearly: after 50 years, we have earned $50m. Wait longer, and the line heads off into the stratosphere, leading us to the misguided conclusion that we need a war-chest of infinite size for our prize.

Pursuit of the positive

One of the first lessons that business school students are taught is that it will be their job, when they emerge into the world of work, to look for initiatives that have positive present values. A machine in a factory will cost a certain amount to acquire and install. It will give rise to various benefits, over a usable life of a few years. Do we think that the present value of the benefits bigger than the cost? Or, to put it another way, is the net present value of the benefits and the costs combined likely to be positive? If it is, buy the machine. If it is not, do not buy the machine.

The same reasoning applies to investing in infrastructure. An airport is for sale. Should we buy it? Yes, if the present value of what we will earn from it exceeds what the seller is asking for the asset.

In infrastructure investing, this is the only consideration. In the buying and selling of stocks and shares, DCF is just one consideration among myriad others which would not cross the mind of an infrastructure investor for a second.

It is the mission of Pier Analysis to make non-specialists in finance familiar with the connection between companies’ current valuations and what those companies need to deliver, by way of cash flow, to justify those valuations.

What next?

If you find this analysis interesting, you can sign up to have others like it delivered to your inbox several times a week.

Share Pier Review with interested friends.

Notes

If you do the division exactly rather than approximately, the figures are not $980,000, but $980,392; and not $960,000, but $961,169.